Global Stocks

Stocks are attractive in the U.S. and several other countries, driven by improvements in economic performance.

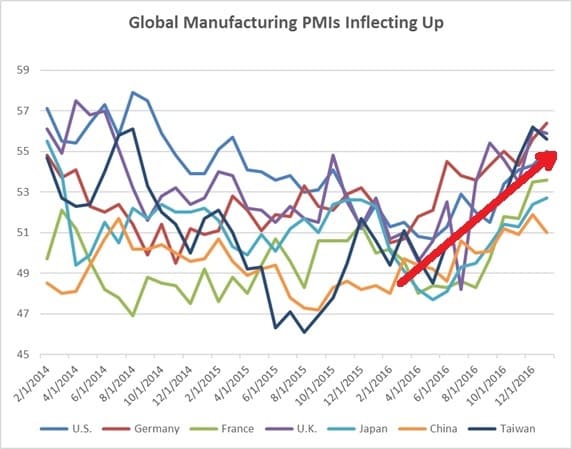

Since the third quarter of 2016, U.S. corporate profits have begun to rise after a six-quarter stint of sideways earnings. Since the end of the first half of 2016, manufacturing PMIs have been inflecting up around the world. (The Purchasing Managers’ Indices survey samples of business managers about their perceived prospects for new orders, inventory levels, production, supplier deliveries, and the employment environment.) Combine this with higher export statistics and expectations for continuing corporate profit growth globally, the advent of modest inflation in much of the world and expectations that global GDP will continue to rise, and it all argues for higher stock prices in many countries.

As we have noted in recent letters, the trend began moving up significantly before the November elections. This is one of several reasons why we believe that the current rally in many global stock markets is being driven not simply by the hope for policy changes, but by underlying economic fundamentals that are translating into growing corporate profits — the mother’s milk of stock prices.

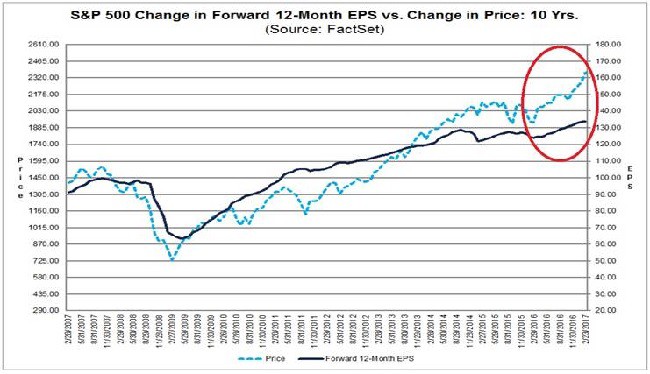

The “earnings recession” that had dogged U.S. stocks since the last quarter of 2014 ended in the third quarter of 2016, and as the chart above shows, the rekindling of earnings growth corresponded with a renewal of the U.S. stock market rally. For the fourth quarter of 2016, S&P 500 earnings grew at an annual pace of 4.9%.

Along with rising PMIs, we anticipate rising inflation in many parts of the world, as well as rising interest rates. (Of course, the global economy is not perfectly synchronized; Brazil, for example, is just now beginning to exit its recent painful recession, and the central bank is expected to be lowering interest rates over the coming year.)

Investment implications: Global PMIs continue the advance they have been enjoying since the middle of 2016. This is one of many points of data we see which suggest that the current rally in many of the world’s stock markets is more than simply anticipation of constructive policy moves from the new U.S. administration. Business is improving — and judging from the current earnings season, corporate profits are likely to follow suit.