The Biggest Transformation of the Next Decade: Disrupting Global Transportation

Gridlock in Washington, whether real or apparent, has slowed the “Trump trade.” Market enthusiasm in the election’s wake focused on the beneficiaries of tax reform, regulatory relief, and infrastructure development, and with progress on those fronts in question, enthusiasm has turned to the other irrepressible stalwarts: the U.S.’ big, disruptive tech companies. The chief suspects here are the likes of Alphabet [NASDAQ: GOOG], Amazon [NASDAQ: AMZN], Facebook [NASDAQ: FB], and Apple [NASDAQ: AAPL]; but there are many others. [Note: Guild owns each of these stocks for some clients; please see our disclosures at the end of this newsletter.]

Market sentiment is favoring these companies for the same reason that we have favored them. Each in their own way, they are relentlessly driven to capture the new opportunities opened by the “fourth industrial revolution.”

If you think about the wealth that was created by disruptors in the first three industrial revolutions, and the pain that came in each transition, you’ll see why investors are so eager to participate, and why these disruptors are a constant focus of our attention.

What Makes the Disruptors Different

For now, the Silicon Valley disruptors who maintain a “Day 1” vigilance and energy are succeeding in one crucial task: they do not think of themselves first as product manufacturers, but as customer satisfiers. As AMZN chief Jeff Bezos noted in his letter to shareholders earlier this month:

“There are many advantages to a customer-centric approach, but here’s the big one: customers are always beautifully, wonderfully dissatisfied, even when they report being happy and business is great. Even when they don’t yet know it, customers want something better, and your desire to delight customers will drive you to invent on their behalf. No customer ever asked Amazon to create the Prime membership program, but it sure turns out they wanted it…”

The disruptors see the potential customer satisfactions that can be created with new technology; and rather than stay fixed in the manufacture of a product by which they define themselves, they freely transform their offerings to give customers what they really want — even if those customers don’t yet know what that is.

The biggest example of this transformation and this disruption that we can see coming in the next decade will be in transportation. Put very simply, Detroit’s big firms identified themselves as car-makers — but the Silicon Valley disruptors who will eat Detroit’s lunch will identify themselves as people transporters. Detroit will keep trying to sell cars, while Silicon Valley will identify and remedy the huge inefficiencies that plague the transportation system, and delight customers in a way Detroit can still barely imagine. (They are beginning to imagine it, and racing to catch up — but history does not bode well for their efforts.)

Source:  Wikipedia

Wikipedia

The Eye of the Storm: Autonomous Vehicles, Ride Sharing, and Yes — Flying Cars

These considerations came into focus for us in the past week with two news items related to GOOG.

First, in GOOG’s first-quarter results, the company announced that ordinary consumers would be participating in real-world testing of its autonomous (that is, driverless) cars. A hundred “early rider” families in Arizona signed up with Waymo — GOOG’s new name for its self-driving car division — to use a fleet of minivans for all their transportation needs. They won’t have a car standing by; they’ll hail one from a smartphone app. For now, these cars will have an engineer present at the wheel and ready to take over operating the vehicle as necessary.

(Second, GOOG chief Larry Page’s Kitty Hawk startup announced the arrival of a flying car. That one was a bit of a disappointment, as it turned out to be not so much a flying car as a flying jet ski — definitely a recreation opportunity rather than a transportation option. But don’t lose heart — there’s hope for your flying car yet, as we’ll discuss below.)

This is not the first deployment of user-hailed autonomous vehicles. Uber Technologies made an abortive attempt to do it in San Francisco last year, before they baulked at California’s regulatory requirements; they also headed to Arizona, where the state authorities have been more accommodating. A similar operation in Pittsburgh met with public opposition sparked by Uber CEO Travis Kalanick’s participation in President Trump’s roundtable of tech entrepreneurs. (Uber has had a number of public relations gaffes and accusations of managerial dysfunction.) Although GOOG and Uber are running the only current public trials of autonomous shared vehicles, many others have announced plans — notably General Motors [NYSE: GM], which owns a stake in ride share service Lyft. Some other major carmakers who at least want to be seen jumping on the bandwagon include Ford [NYSE: F], Peugeot [France: UG], Volkswagen [Germany: VOW], BMW [Germany: BMW], Volvo [Hong Kong: 0175], and Renault [France: RNO]. Many of them are making deals to cooperate with local authorities in the U.S., Europe, and China.

The flood of deals and announcements made starting in the second half of 2016 suggests to us that the technology may be accelerating more than the market appreciates. And that spells major disruption for global transportation — as major as the arrival of the railroads, and as major as Henry Ford’s mass production of the Model T.

Technology and Economic Reality Will Eat Your Car

Here’s why change is inexorable.

One: The world’s fleet of light vehicles is an incredibly inefficient use of capital. The average vehicle is in use less than an hour a day, a utilization rate of 4%. But the average vehicle can carry five passengers, and on an average trip carries only 1.5. So the real utilization rate of available seat-miles is just over 1%. The reason that ride-sharing services such as Uber and Lyft have gained such rapid traction is that they are grabbing the low-hanging fruit in remedying that inefficiency.

Instead of thinking about a market for cars, the way Detroit does, Silicon Valley thinks about providing satisfying passenger miles to customers. And Silicon Valley’s technology can push down the price of passenger miles by an order of magnitude.

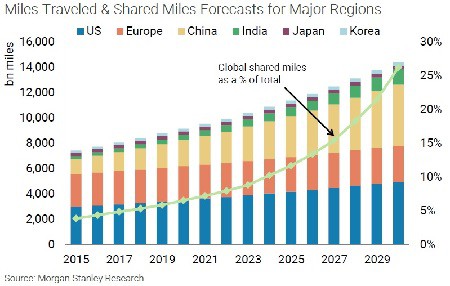

In four years, Uber has gone from no share in global light vehicle passenger miles, to a 0.4% share. At 1.7%, its size would rival Toyota [NYSE: TM]. Some analysts expect ride sharing miles to be 25–40% of the global total by 2030.

We do not suggest that Uber will capture all that share: the history of tech disruptors is littered with companies which crashed and burned due to management missteps and other problems and never realized their potential. But if it isn’t Uber, it will be someone else.

Two: Driving is a vast waste of time, and therefore money. With global light vehicle traffic covering 10 trillion miles a year at an average speed of 25 miles per hour, that’s 400 billion person-hours of time spent behind the wheel of a car (600 billion if you include passengers). The value of that time is part of the opportunity cost of the current system of private car ownership. At $10 an hour, it equals about 5–8% of global GDP. (You can decide whether that $10 figure is accurate for yourself.) And of course, even in a ride sharing situation, paying the driver for his or her time accounts for about half the cost of a passenger mile.

Further, with more than a million road deaths a year worldwide, most caused by human error, the reality — as uncomfortable as it may be for us proud humans to admit — is that robot cars will on the whole be a lot safer. High profile events notwithstanding, Tesla Motors [NASDAQ: TSLA] has already noted a 40% decline in accidents involving their models equipped with advanced driver assistance technologies. (And if you think humans won’t accept this reality, ask yourself how many friends you have who prefer an abacus to a calculator.)

Phones and Robots

Two suites of “fourth industrial revolution” technology make this situation ripe for disruption. First, smartphones and the internet make ride sharing feasible — that’s the first layer and the low-hanging fruit. Second, artificial intelligence and robotics are now on the cusp of removing the need for a human driver. This second item is not years away; it is being deployed now. The fundamental challenges are no longer technical; they are social and political. And although history has shown that social and political challenges can slow the adoption of technologies that improve human life, history also shows that they ultimately will fail to stop it.

Together, these add up to what some analysts refer to as “shared autonomy” or “Auto 2.0.”

With Uber and GOOG’s early public trials, the future is coming into view: a world in which transportation is an on-demand utility no longer bound to personal ownership of a given product, such as a car. You will press a button on your phone, and a robot car will appear and take you where you want to go. We emphasize again that this is not hopeful science fiction: it’s actually happening today in Phoenix. (From one perspective, this is what it looks like when private enterprise provides public transportation.)

The pace of adoption will vary widely by geography and with political and economic factors, as California already discovered when GOOG and Uber centered their public debuts in Arizona. But the shift will be driven, in the end, by the more rational economics of shared autonomous vehicles, which will give customers what they want at a price they love.

Implications

The implications of this shift are legion. Obviously, light vehicle manufacturers are front and center in the line of fire. They are late to the game, and they lack the dynamic “Day 1” corporate culture of their Silicon Valley competitors. Their public efforts could be more spectacle than substance, though both F and GM are deploying significant resources to the effort. These incumbents have enormous capital, and should be watched. Rental car companies are already under pressure from ride sharing, and that pressure will not be relenting.

Notably, the move to shared autonomy may accelerate the adoption of electric vehicles, with potentially significant implications both for manufacturers and for global oil demand. While electric passenger vehicles typically have a fuel cost per mile of about 3 cents, versus 7.5 cents for an internal combustion engine, electric vehicles cost more up front. Right now, the payback period to benefit from the lower fuel costs can be 30 years. But as shared autonomous vehicles raise the utilization rate, that payback period could quickly drop to 2 or 3 years. This positive feedback loop of intersecting technologies could result in market changes of surprising speed and magnitude.

And finally, we would be remiss not to offer you your flying car. With all respect to the fun time that Larry Page’s baby could offer you over a lake in northern California, have a look instead at the eHang 184 — a single-passenger autonomous drone scheduled to begin testing in Dubai this summer, and in the U.S. by 2020. (eHang is a private company headquartered in Guangdong, China.)

And finally, we would be remiss not to offer you your flying car. With all respect to the fun time that Larry Page’s baby could offer you over a lake in northern California, have a look instead at the eHang 184 — a single-passenger autonomous drone scheduled to begin testing in Dubai this summer, and in the U.S. by 2020. (eHang is a private company headquartered in Guangdong, China.)

Source: Xinhua

Uber Technologies has established a division called “Elevate,” which last year published a white paper called Fast-Forwarding to a Future of On-Demand Urban Air Transportation.

We know you’ve been waiting since The Jetsons, but with all due caution, this looks like the real deal.

Investment implications: Even contrarian investors should be cautious when they look at the shares of big auto manufacturers: they may be cheap for a reason, and that reason may become clearer in coming years. Nevertheless, just as it would be foolish to count out Wal-Mart [NYSE: WMT] in the battle with AMZN, investors should monitor the shared autonomy plans of GM, F, and others. The growth of shared autonomy will mean that passenger miles will be growing significantly faster than vehicle sales in the long run. At this juncture, we like the big, disruptive U.S. tech stocks that we have mentioned, and we caution investors that technological promise does not mean that any stock is selling at a rational or desirable price. Some automotive equipment manufacturers, although not pure plays, may offer exposure to the theme of autonomy, such as Magna International [NYSE: MGA] and Delphi [NYSE: DLPH]. TSLA is an obvious participant, both in shared autonomy and in the growth of electric vehicles and in battery technology; we would look for a rational entry point for TSLA shares. Finally, the potential inflection of electric vehicle sales in coming years suggests that investors look closely at lithium producers, and oil investors should consider and monitor the longer-term demand implications of these new technologies.