At the end of March, we noted about the dollar:

“In [the context] of a very likely European recession, regardless of the cessation of hostilities in Ukraine, we would expect the U.S. dollar to stage a stronger rally, particularly against the euro. Why isn’t it? And perhaps a question equally as sharp: If this is the best the dollar can manage under conditions that we’d imagine are so favorable to it, how could it behave under unfavorable conditions?”

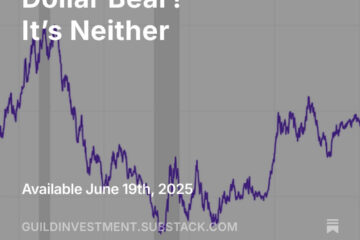

Well, what a difference a few weeks make. Since we wrote, the dollar has put on a strong rally, with the DXY index — the index that sets the U.S. dollar against a basket of other major global currencies, primarily the euro and the yen — rising more than 5% in short order.

DXY Dollar Index — Year-to-Date 2022

Source: Bloomberg LLP

As noted above, the largest currencies in the DXY basket are the euro (58% weight) and the yen (14% weight). Both of these currencies are under intense pressure for very different reasons — different reasons which illustrate how current global conditions represent a “perfect storm” of disparate converging forces operating in favor of the dollar.

Europe is under pressure because of a likely imminent recession brought on by spiking inflation and an economic slowdown courtesy of Russia’s war in Ukraine and the effect it has had on commodity prices — especially, where Europe is concerned, natural gas, fertilizer, and food. Despite European leaders’ efforts, the united front against Russian demands for ruble gas payments is already cracking, with some countries, and major companies in Germany and Austria, agreeing to pay for gas in rubles. This demonstrates how toothless European foreign policy is in the face of the bloc’s dependence on Russian energy. German industrial unions have been willing to state publicly what everyone knows — namely that without Russian gas, Germany would be plunged into a depression. All of this means poor demand for the euro. (It has also put the ruble back to its pre-invasion levels.)

Meanwhile, in Japan, the central bank remains dedicated to its yield curve control, which is keeping it on an easing path out of step with the desperate turn to tightening by the U.S. Fed and much of the rest of the developed world. The yen is therefore weakening at a historically rapid pace.

Thus far, these phenomena, as fast as they have been, have not created a systemic problem. Currency instability — particularly when it is large, globally important currencies used in many international financial trades and transactions — is of particular concern to financial authorities. Currency shocks — such as the Chinese yuan devaluation of 2015 — can have deleterious effects on global financial markets, so we are watching closely. Of course, the Fed and the U.S. Treasury are also watching closely and communicating with their counterparts in Japan. Until there is some threat of instability, however, we think U.S. officials will be content to watch the dollar benefit from the yen’s and euro’s woes, as a stronger dollar blunts the force of inflation in the U.S.

Still, this is one of the items we note as something that might convince the Fed to pause its tightening in the event of systemic instability.

Meanwhile, in China, which last sparked financial consternation with its sudden yuan devaluation in 2015, yuan weakness is likely as the country continues to pursue its “zero covid” policy in the face of the fast-spreading omicron variant. This policy has not worked elsewhere, and given the ease with which omicron spreads, will not work in China; but it will weaken the Chinese economy and the Chinese currency. So will other converging pressures on China: for example, its relations with Russia in the face of global sanctions; the ongoing prospect of conflict with the U.S. over Taiwan; even trouble in its over-leveraged property sector; and so on.

It’s the 10-Year, Stupid

For U.S. investors, we believe that rising rates and tightening domestic financial conditions remain the real, central backdrop of their investment decisions. The rising dollar, as we noted above, blunts some of the force of inflation, and slightly reduces the pressure on the very late-acting Fed to raise rates precipitously. On balance we believe this upward pressure on the dollar is likely to continue: the war in Ukraine is grinding on without resolution as weapons pour in from the west; Japan remains dedicated to maintaining its yield curve control, and thus it is committed to its easing path.

As we have said for years to those who suggest the dollar will collapse due to U.S. fiscal intransigence — collapse compared to what? There is still no competition, so collapse is not in the cards in the foreseeable future.

In terms of fiat currencies, for now the dollar remains “the cleanest dirty shirt in the laundry.” Collapse is not in the cards, but tightening is. Thus far we can see little that will immediately derail the Fed’s plans, which will become more concretely outlined after the May 5 meeting of the FOMC. The Fed funds rate needs to rise a lot to get to where it should be — and it will probably not get there. But already, the 10-year Treasury is reaching a key level — it is approaching 3%. Historically, 10-year yields under 3% have seen 21.9% annualized U.S. stock market returns, while yields over 3% have seen 10% returns. Since 1950, when rates were under 3% there has been only one bear market; but there have been 10 when rates were above 3%. The 10-year is currently at 2.8%.

The simple reality is that inflation is constraining the Fed finally to act, and to act fast. There are many factors now converging to drive inflation, even though dollar strength is relieving some of the bite (including supply chain issues, embedded labor cost inflation, and commodity inflation). Inflation is likely to remain persistently high for years — perhaps 4 or 5% — even if it falls back from the current peak. So we can look forward to 10-year rates decisively crossing the historically significant 3% threshold, and we can look forward to the consequent contraction of the “aspirational” (read: excessive) valuations in many long-dated assets.

Naturally, a corollary of this is that those who can avoid bonds in their investment allocation should do so. The decline experienced thus far by bondholders does not yet give a clear picture of how bad we believe it could get. One analyst we read recently noted that many credit strategists are “preferring to take default risk over duration risk.” In layman’s language, that means that they would rather own short-term junk than long-term quality — because they’ll be out of the short-term junk quickly, but the long-term bonds, even if they are high quality, will be crushed by rising rates. In our view, those who must hold bonds should pay attention to both duration and quality and not reach unduly for yield.

We have little doubt of three summary points:

- Investors will flock to growth as a reasonable at a reasonable price (GARP). This is a value style that works well in a period when a recession may be in the future. First quarter US GDP just gave a negative 1.3% print — one more down quarter and a recession will be confirmed.

- Market PE ratios will continue to decline to to historical norms relative to growth.

- Over-owned former growth companies that have lost their growth mojo will be harshly punished. Netflix [NFLX] is an example.

Intelligent investors will work to find companies that fit the right investment parameters and will consider interest rate risk, foreign exchange risk, stagflation risk, labor costs, supply lines, and many other variables. They will not flock to passive stock market indices.

Investment implications: Rising rates are certain to compress stock market multiples as well as hurt bonds — spelling trouble for the ubiquitous indexed 60/40 stock/bond portfolio that has become a retirement-account staple over the past two decades, and which has shown significant weakness year to date. We expect to see the return to a PE ratio of less than 20 for the S&P 500. We expect to see much lower PEs for for those companies expected to have no earnings for four or five more years. In fact, the question remains: How many of these companies will actually survive the current bear market?