More Evidence the Inflation Spike Is In the Rear View Mirror

PPI (producer price inflation) data yesterday showed slowing inflation impulses, as we have discussed. Even our own index of basic essential needs (representing food, clothing, shelter, and energy components) reflect a sharp slow down in price increases from this past summer’s record levels. After hitting a year-over-year high of over 40%, the October YoY increase is only 5.8%.

Mixed Results Leave Investors Scratching Their Heads

Earnings season concludes with a lot of disparate data for investors to digest. Q3 2022 numbers were good, but — as we mentioned in last week’s Zoom call — the Q4 2022 and 2023 guidance included a lot of downbeat commentary. Retailers are the last to report, and their results this week have been quite varied, not unlike so many other sectors where individual company results and outlooks offered mixed signals. A few anecdotes from some companies highlighted a marked economic slowdown in October, and a few retailers warned that it may be continuing into November. This has caused people to remove some of the Fed tightening from their expectations… and has removed the upward trajectory of the very strong USD. We reiterate that if the dollar has peaked, and inflation remains elevated, look for good companies with pricing power to turn higher revenues into higher earnings… without the currency headwinds of 2022.

It is a busy time of year. Last week’s Zoom call we mentioned that when much anticipated events happen, buyers who have been waiting…. buy. Seasonally, we are in a good period for market rallies. Many stocks have fallen a lot and there is still money on the sidelines to buy stocks, so the market can do well in spite of fears of a recession and earnings cuts that may be in store for 2023. However, noise levels about 2023 weakness is increasing. The economic data calendar between now and the next Fed meeting in mid December is heavy. The number of Fed speeches in the coming weeks is also high. We expect traders to treat the data and headlines with quick impulses and act in a manic manner. So, while the seasonals are supportive, few market participants believe we are starting a new bull market, so much of the buying being done is lower conviction buying, or just trading.

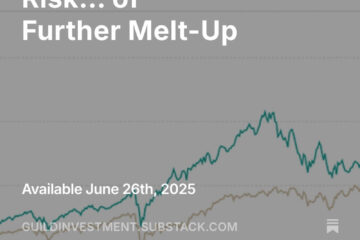

The S&P 500 has not been able to recover its 200-day moving average, nor bounce 50% of the 2022 decline, but is trying.

Source: Bloomberg, LLP

The odds favor the market doing very little on the upside in the next few weeks, and the onset of a recession in 2023 will be monitored by every economic pronouncement between now and the end of April. There are reasons to believe that a recession will be very serious in 2023, and reasons to believe that it will be very mild. We are in the camp of a medium-severity recession between these extremes. That means corporate profits will continue to fall — perhaps by 15% or more in 2023. This makes high P/E stocks very vulnerable, and it makes low P/E stocks relatively attractive. We expect leadership to continue to move from high-P/E tech stocks with glorious potential to low-P/E bargains that can be found in several sectors of the economy. This is where we will focus our attention. Be aware that some stocks are low P/E because they have absurd price appreciation in the commodities they produce. This price appreciation in the commodities will diminish, which makes chasing low-P/E commodity stocks dangerous.

Thanks for listening; we welcome your calls and questions.