Since the pandemic broke, it’s been apparent to us — as it has to many other investors — that the virus would bring significant social and economic change in its wake. The post-covid world would be different from the pre-covid world, and those changes would benefit some sectors, industries, and companies, and impair others. Some of these changes may prove to be transient, but many will not. We believe investors would be wise to take account of the lasting changes as they position their portfolios for growth in coming years.

This week we’ll begin a series of brief reflections on where we believe the most significant and lasting changes will occur, beginning with the related themes of e-commerce and financial technology.

Even a cursory glance at the U.S. stock market after the March pandemic panic lows shows the strong outperformance of e-commerce stocks. Most of us who have been in some form of “shelter in place” for the past several months can understand why the stock of Amazon [NASDAQ: AMZN] is at all-time highs: either we have been relying on AMZN for the delivery of necessities, or we’ve seen our neighbors’ gates and doorsteps piled with AMZN packages.

The theme is obvious. The question is whether it is durable, and in our view, it is. Why? And what other beneficiaries could there be?

First, e-commerce is benefitting from virus-related cultural changes that will last for some time. “Shelter in place” and fear of the pandemic among some of the population have created anxiety about the risks posed by exposure to high population density areas and activities. Even as the acute sense of covid risk gradually declines, there will likely be a lasting hangover in an incremental consumer shift to more home- and family-based activities, consumption, and entertainment.

First, it is far from a “done deal” that an effective vaccine will ever be developed. Of course there are those on both sides of the argument; experts such as Dr. Fauci believe one will be available by early 2021. However, we note that no effective vaccine has yet been developed for a coronavirus, despite decades of research. And second, the experience may plant in consumers’ minds the realization that emergent, novel zoonotic (animal-derived) viruses are likely to become more common as humans increasingly impinge on the remote areas where their reservoirs have until now existed undisturbed. All of this helps explain the early signs of a possible exodus from some cities towards the suburbs.

Second, there has been ample policy support for wage earners. Unemployment spiked, and may to some extent prove stubborn. However, it is already showing signs of a remarkably rapid recovery. (Remote work technology has also made it easy for a significant portion of the workforce to work from home.) And finally, fiscal support for workers has been robust — both unemployment benefits and loans to employers to keep employees on payroll. We suspect that as long as the effects of the “shortest recession” linger, these support mechanisms will persist to a greater or lesser degree.

Taken together, this all means that consumers have money to spend, and fewer places to spend it — but plenty of opportunity to spend it online.

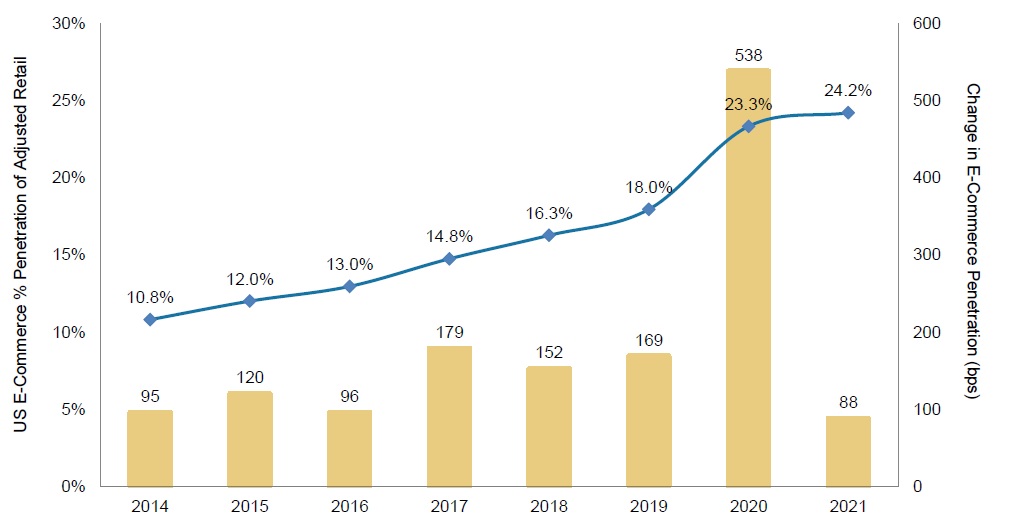

Indeed, not only has the accelerated shift to e-commerce not run its course, by some metrics it is only getting started. In April, analysts estimate $170 billion in consumer spending up for grabs as consumers sheltered in place and didn’t spend on restaurants, bars, and brick-and-mortar retail. E-commerce only captured 12% of that total.

It’s estimated that in spite of government support, many thousands of brick-and-mortar retail establishments could permanently close this year, shrinking another vector for offline consumer spending. Even if e-commerce secured only 4% of the consumer spending that’s estimated to be lost by offline retail in the second half of 2020, that would lead to a torrid 25% expansion rate for the full year. The e-commerce growth trend will probably eventually normalize, but after a “step up” to a higher level, leading to increases in out-year estimates for the industry moving forward.

AMZN is the first beneficiary that most investors consider, but others may include eBay [NASDAQ: EBAY] (which grew its business 20% in April, the first increase since the last quarter of 2018), Shopify [NASDAQ: SHOP], Etsy [NASDAQ: ETSY], Chewy [NASDAQ: CHWY], Walmart [NYSE: WMT], and Wayfair [NYSE: W]. In this context investors may also note the emergent e-commerce platforms of Facebook [NASDAQ: FB] and Alphabet [NASDAQ: GOOG], which are expanding “social commerce” strategies that may help shape their offerings into enticing one-stop promotional venues for small and mid-sized businesses.

The same “step up” in the curve of e-commerce growth that we observed above may also been seen in electronic payments. The transition to online spending has immediate obvious benefit to Paypal [NASDAQ: PYPL] and Square [NYSE: SQ], as well as the card networks such as Visa [NYSE: V] and Mastercard [NYSE: MA]. Many consumers will have established digital wallets and contactless payment solutions during the shelter-in-place period, and both ongoing caution about hygiene, and enjoyment of digital payments’ ease of use, will likely make this adoption “sticky.” We note particularly the penetration of payments via digital wallets, contactless cards, and other fintech solutions into low-value transactions that have until now been predominantly cash. Analysts expect card spending to track 4–6% above overall consumer spending, accelerating the sidelining of cash and checks.

Investors should not neglect the value add of Apple Pay [NASDAQ: AAPL] and Android Pay [GOOG] to those companies’ ecosystems. The pandemic might prove to be a watershed in accelerating digital wallet use in the developed world. We would also be remiss not to mention business-to-business payments, an area that has until now been a particularly tough nut for fintechs to crack. Coupa Software [NASDAQ: COUP], which specializes in business spend analysis, may be well-positioned to take share in this area if the current trend of business digitization continues to accelerate.

Investment implications: Some of the e-commerce and fintech beneficiaries of covid-driven change that we have mentioned are now quite richly valued on a forward earnings basis. We believe that the themes from which they are benefitting will prove to be enduring. We also believe that the stock market is likely to be marked by significant volatility as the pandemic progresses and changes, and as more vigorous campaigning gets underway ahead of November’s elections. Ebbs and flows of news around these, as well as other unforeseeable events both nationally and globally, may create opportunities to buy stocks with exposure to e-commerce and fintech themes at more attractive prices — so we advise investors to have a ready buy list. November election outcomes may suggest changes of trend — but that is a topic we will cover as November’s political landscape becomes more visible over coming months.

Please note that principals of Guild Investment Management, Inc. (“Guild”) and/or Guild’s clients may at any time own any of the stocks mentioned in this article, and may sell them at any time. In addition, for investment advisory clients of Guild, please check with Guild prior to taking positions in any of the companies mentioned in this article, since Guild may not believe that particular stock is right for the client, either because Guild has already taken a position in that stock for the client or for other reasons.