We all know that markets can climb walls of worry and brush off bad news even while the front pages scream about war and sanctions, and contrarian pundits worry about (or gloat over) the prospect of dollar collapse. The past several months have been a textbook illustration. The conflict with Iran grinds on with whiplash announcements of on/off peace deals, the Strait of Hormuz — that narrow waterway through which roughly a fifth of the world’s seaborne oil passes — remains under naval blockade; and yet the S&P 500 has rallied, the dollar has held firm, and corporate earnings have come in stronger than expected. The temptation is to call this complacency; a more accurate reading may be that durable forces are doing the heavy lifting beneath the daily noise.

The Dollar Remains a Superpower

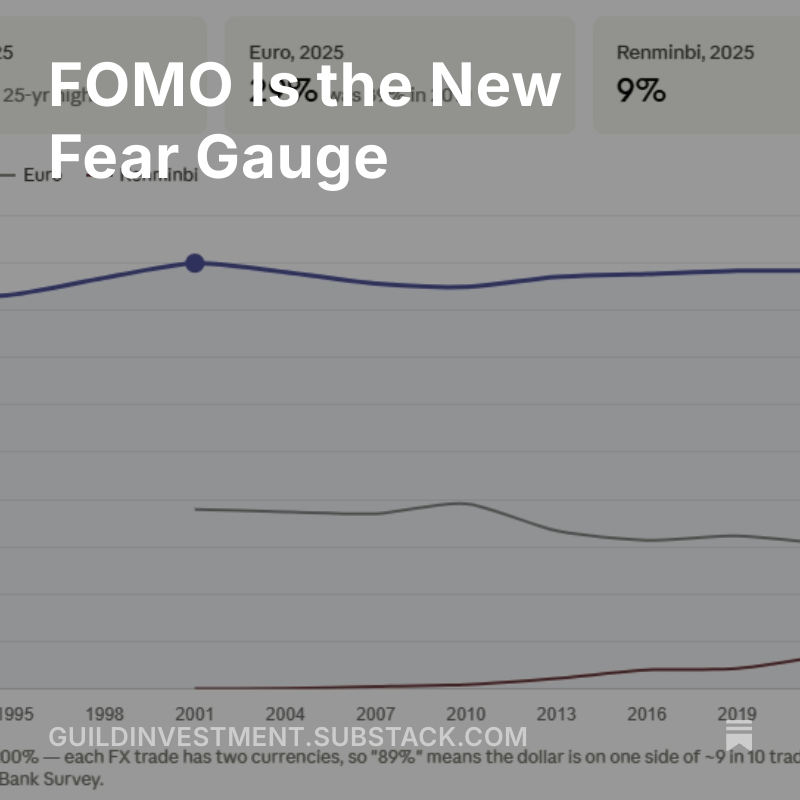

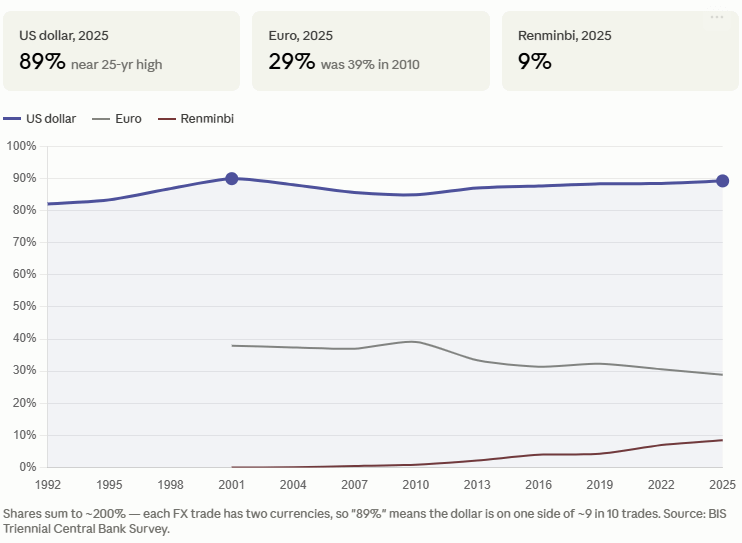

Every few years, a fresh geopolitical shock revives predictions that the U.S. dollar is about to lose its perch ruling the roost of global currencies. The “petrodollar” theory gets trotted out: take away oil pricing in dollars, the argument goes, and the whole edifice topples. It is a convenient story for doomsayers, but it inverts cause and effect. Oil producers chose to price in dollars because the dollar was already the common yardstick against which most prices, contracts, and values are quoted — for a host of reasons which have not fundamentally changed, including U.S. military and blue-water naval hegemony as well as the unchallenged role of the U.S. as a preeminent destination for global capital seeking the rule of law and the productivity that comes with it. The petrodollar was a consequence of dollar dominance, not its source, even if its development served to cement that dominance still further.

The real engine is the network effect. Daily turnover in foreign-exchange markets runs roughly $9.6 trillion. Global merchandise trade for a full year is about $40 trillion. In other words, the FX market churns through a year of global trade every four days — and the dollar appears on one side of about 89% of those transactions. Dislodging that would require, as we have observed for years, not merely an alternative currency or alternative currency transmission rails — but an alternative legal system as generally predictable as that in the U.S., an alternative capital market as deep as that in the U.S., and an alternative security architecture as effective as the global umbrella provided by the U.S. None of those exist today; and none look close to viability in the near or mid-term future.

What about a more distant future — are there cracks showing there? The freezing of Russian sovereign reserves in 2022 reminded every central banker that dollar assets are, in the end, held at Washington’s pleasure. Central banks have been buying gold at an accelerating pace and broadening their geographic mix of reserves. Countries are quietly building alternative payment rails. However, none of this threatens the dollar tomorrow, the day after tomorrow, or frankly for decades to come, if ever. But it is worth watching, because the dollar’s status is the silent assumption underneath almost every portfolio decision an American investor makes.

The Ratchet Effect

If the dollar is the foundation, the second pillar is the asymmetric way stocks process news. Good news, or even the hint of it, is reason to rally. Anything short of unmistakably bad news gets a shrug when animal spirits are present and growth projections are moored in some approximation of sanity and sobriety. Markets ratchet upward.

We believe great financial advice starts with truly understanding your goals, needs, and circumstances. Schedule a meeting with our Client Relations Director to discover if Guild Investment Management has a solution that will work for you.

A vivid example arrived recently when reports of a U.S.–Iran deal to reopen the Strait of Hormuz sent S&P 500 futures up about 1% over a single weekend and dropped Brent crude more than $8 a barrel. When fresh strikes followed and the deal looked wobbly, stocks gave back only about half of those gains. “Heads I win a dollar, tails I lose fifty cents” repeated thousands of times, creates bull markets.

The VIX — an index that measures the market’s expected swings in the S&P 500 over the coming month, often called the “fear gauge” — has been sitting in the comfortable lowlands of the low-to-mid teens. More interestingly, the usual skew in options pricing, where downside protection costs more than upside participation, has flattened. Institutional investors are buying upside call options as “FOMO insurance” — hedging against the risk of missing a tech-led rally rather than against a crash. When the fear gauge mostly measures the fear of being left behind, you have a sense of the prevailing mood.

Earnings Doing the Work

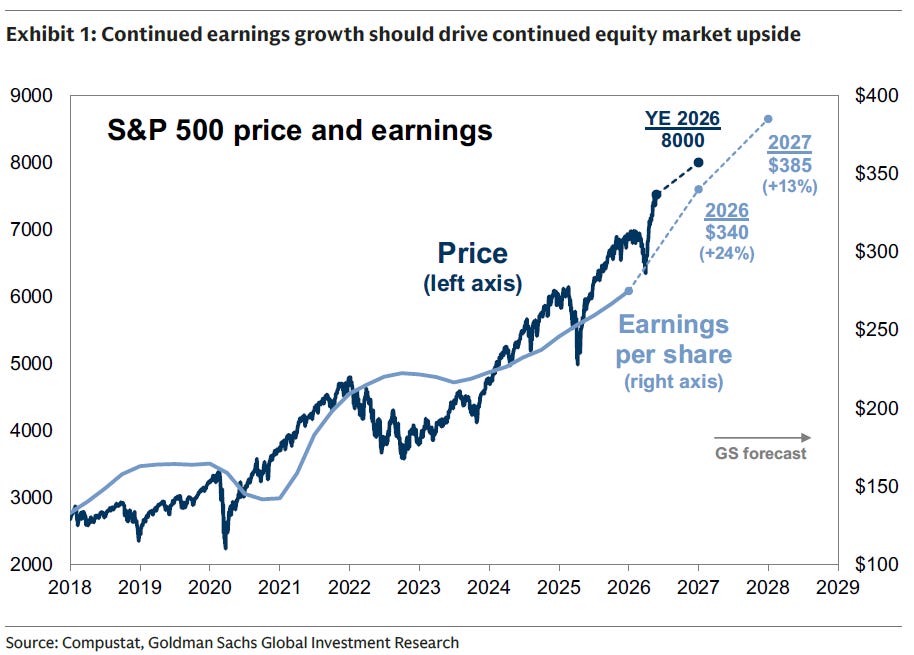

So far this year, the S&P 500 is up roughly 10%, but forward earnings estimates have risen about 15%, meaning the forward price-to-earnings multiple (a stock’s price divided by the profits it is expected to generate) has actually declined slightly. Investors are getting more future earnings per dollar of stock investment than they were in January, assuming that forward estimates are not getting fantastical. (This is an assumption one can examine critically, but it is not a heroic assumption.)

Major Wall Street strategists are projecting S&P 500 earnings near $340 per share in 2026 — up roughly 24% year-over-year — and around $385 in 2027, with year-end index targets in the neighborhood of 8000 (Goldman recently reaffirmed theirs). Roughly half of that growth is being delivered by companies tied to the artificial-intelligence build-out: the chipmakers, the hyperscalers (the handful of cloud giants like Amazon, Alphabet, Meta, and Microsoft that are spending hundreds of billions on AI infrastructure), and the power and grid companies feeding electricity to data centers.

This is quite different from past concentrated rallies, as analysts have been pointing out for some time. The late-1990s episode was a multiple-expansion story — prices ran far ahead of profits. This one is a profits story, with prices roughly keeping pace. That does not make stocks cheap, since valuations remain elevated relative to long-run history, but it makes the bull case much more defensible.

What It Means for Portfolios

Do not bet against the dollar because of geopolitical theatrics as analyzed by “permabears”; the network effects supporting it are far deeper than headlines suggest. Keeping out of a market a market that “wants to go up,” as the old tape-readers say (and this one manifestly does “want to go up”) is a humbling exercise, and don’t forget that being chronically underexposed is itself a risk. The earnings story argues for owning the AI build-out, but with some discipline: the hyperscalers and power-infrastructure names have, on the whole, lagged their own earnings growth, while many semiconductor valuations have run ahead. And because so much of the index now leans on a handful of AI-linked names, balancing the portfolio with companies that have strong earnings momentum but minimal AI sensitivity — selected names in energy, materials, and perhaps health care come to mind — is prudent diversification. Of course, as is always the case, a correction could come at any time; if the established backdrop holds, we would regard such a correction as an opportunity to gain or deepen exposure to our favorite themes and ideas.

Thanks for listening; we welcome your calls and questions.

General Disclosures About This Newsletter

The publisher of this newsletter is Guild Investment Management, Inc. (GIM or Guild), an investment advisor registered with the Securities and Exchange Commission. GIM manages the accounts of high net worth individuals, trusts and estates, pension and profit sharing plans, and corporations, among other clients.

Your receipt of this newsletter does not create a personal investment advisory relationship with GIM although some recipients may also be advisory clients of GIM. GIM has written investment advisory agreements with all its personal advisory clients, which sets forth the nature of that relationship.

The newsletter makes general observations about markets and business and financial trends and may provide advice about specific companies and specific investments. It does not give personal investment advice tailored to the needs, objectives, and circumstances of individual readers. Whether investment ideas and recommendations are suitable for individual readers depends substantially on the personal and financial situation of that reader, which GIM, as the publisher of the newsletter, makes no effort to investigate.

GIM attempts to provide accurate content in its newsletters to the extent such content is factual rather than analysis and opinion, but GIM relies primarily on information compiled or reported by third parties and does not generally attempt to independently verify or investigate such information. Moreover, some content and some of the assumptions, formulas, algorithms and other data that affect the content may be inaccurate, outdated, or otherwise flawed. GIM does not guarantee or take responsibility for the accuracy of such information.

Please note that investing in stocks, other securities, and commodities is inherently risky, and you should rely on your personal financial advisors and conduct your own due diligence in connection with any investment decision.

A Special Comment for Guild’s Clients

If you are an investment advisory client of GIM who is receiving this newsletter, please note that the fact that a general recommendation is made of a particular security, commodity, or investment area to its newsletter subscribers does not mean that investment is suitable for you or should be purchased by you. For example, GIM may already have purchased such securities on your behalf or purchased securities in the same industry (and an increase in the position for you may represent too much concentration in one security or industry), or GIM may believe the investment is not suitable for you based on your risk tolerance or other factors. If you have questions about the recommendations in this newsletter in relation to your account at GIM, please contact Tony Danaher, Rudi von Abele, or Aubrey Ford.

Conflicts of Interest

As of the date of this newsletter, GIM’s investment advisory clients or GIM’s principals owned positions in areas that are the subject of current recommendations, commentary, analysis, opinions, or advice, contained in this newsletter.

GIM and its principals have certain conflicts of interest in its relations with its investment advisory clients and its newsletter subscribers resulting from GIM or its principals holding positions for its clients or themselves which are also recommended to its clients. GIM may change the positions of its clients or GIM’s principals may change their positions (increasing, decreasing, and eliminating them) based on GIM’s best judgment at any given time, including the time of publication of the newsletter. Factors that lead GIM to change or eliminate its positions may include general market developments, factors specific to the issuer, or the needs of GIM or its advisory clients. From time to time GIM’s investing goals on behalf of its investment advisory clients or the personal investing goals of GIM’s principals and their risk tolerance may be different from those discussed in the newsletter, and the investment decisions made by GIM for its advisory clients or the investment decisions of its principals may vary from (and may even be contrary to) the advice and recommendations in the newsletter.

In addition, GIM or its principals may reduce or eliminate their positions in an investment that is recommended in the newsletter prior to notifying the newsletter subscribers of such a reduction or elimination. The publication by GIM of a “target price” or “stop loss” for a particular security or other asset does not necessarily represent the price at which GIM intends to sell or will sell any such assets for its advisory clients or the price at which GIM’s principals intend to sell any such assets.

As a consequence of the conflict of interest, GIM’s clients or principals may benefit if newsletter subscribers purchase assets recommended by GIM since it could increase the value of the assets already held by GIM’s investment advisory clients or GIM’s principals. On the other hand, GIM’s principals and clients may suffer a detriment if they seek to acquire additional shares in securities that have been recommended and the price of the securities has increased as a result of purchases by newsletter subscribers.

To help mitigate these conflicts, GIM seeks to avoid recommending the securities of individual companies where GIM or its principals have an ownership position and where the issuer is small or its securities are thinly traded. That way sales by GIM in advance of possible sales by newsletter subscribers would not be likely to cause any significant decrease in the sale price to newsletter subscribers. GIM has a fiduciary relationship with its investment advisory clients and cannot agree on behalf of such clients to refrain from purchases or sales of a security mentioned in the newsletter for a period of time before or after recommendations for purchases or sales are made to its newsletter subscribers.

GIM encourages you to do independent research on the securities or other assets discussed or recommended in the newsletter prior to making any investment decisions and to be especially cautious of investments in small, thinly-traded companies, which are usually the most risky investments that you can make.

Disclaimer of Liability

GIM disclaims any liability for investment decisions based upon recommendations, information, or opinions in its newsletters. GIM is not soliciting you to execute any trade. Nothing contained in GIM’s newsletters is intended to be, nor shall it be construed as an offer to buy or sell securities or to give individual investment advice. The information in the newsletter is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation, or which would subject GIM to any registration requirement within such jurisdiction or country.

COPYRIGHT NOTICE

Guild’s current and past market commentaries are protected by U.S. and international copyright laws. All rights reserved. You must not copy, frame, modify, transmit, further distribute, or use the market commentaries, without the prior written consent of Guild. This email or any download from a secure website is meant for only the intended recipient of the transmission, and may be a communication privileged by law. If you received this email in error, any use, dissemination, distribution, or copying of this email is similarly prohibited. Please notify us immediately of the error by return email and please delete this message from your system. Although this email and any attachments are believed to be free of any virus or other defect that might affect any computer system into which it is received and opened it is the responsibility of the recipient to ensure that it is virus free and no responsibility is accepted by Guild Investment Management for any loss or damage arising in any way from its use.

0 Comments