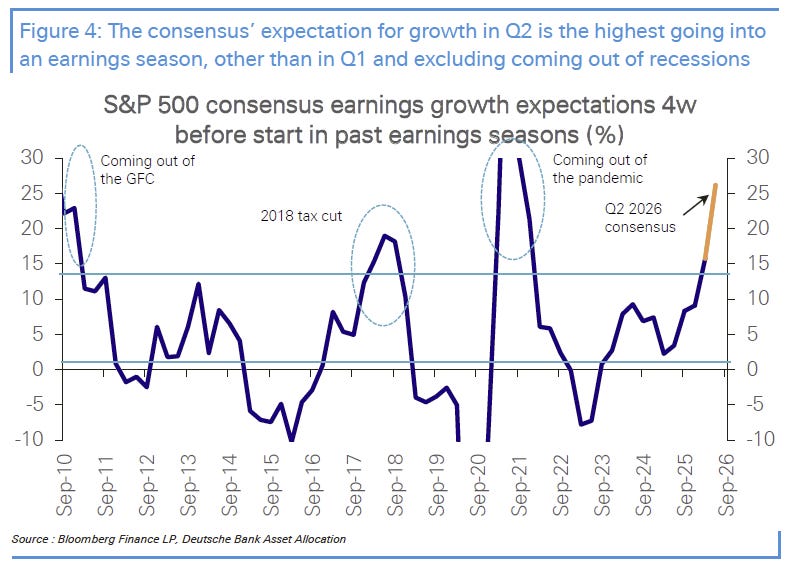

We were surprised to read that Wall Street has never carried higher expectations into an earnings season than it is carrying into this one — recession rebounds aside. The bottom-up consensus (that is, analysts’ company-by-company estimates, added up) calls for S&P 500 earnings to grow 26.2% from a year ago, more than double the old record for a season’s opening expectations (set, by the way, in 2013). Analysts, who normally trim estimates as reporting season gets imminent, raised them 4.4% instead.

Of course, to an extent, beats are nearly automatic anyway, as companies and analysts aim for a “meeting of the minds” that will allow for predictable but moderate beats. A routine set of beats, even good ones, is not news. What investors want to know now is what managements say during earnings about the quarters that haven’t happened yet.

This of course is why we listen to earnings calls; here are five things we (and the Street) will be listening for.

One — Top Line Growth

Last week the big banks, always early reporters, told us that the American consumer looks unambiguously healthy. Card spending rose 10% from a year ago, accelerating from 7%; loan growth quickened; loan write-offs fell; and all four large banks cut the share of their loan books held in reserve. Reserves are a bank’s forecast of its own customers’ potential losses, and the forecast just got sunnier. Now the broader question is breadth: outside mega-cap tech and the semiconductors, the remaining 71% of index earnings is expected to demonstrate growth of about 14% — after contributing almost nothing in 2024 and 2025 — helped by manufacturing activity at a four-year high. (Remember our discussion of AI as an industrial catalyst last week?) Watch the beat rate beyond technology: for the first time in three years, the other 71% of the index is expected to pull real weight.

Two — Margin Expansion

More companies each quarter credit AI adoption for expanding profit margins, and some are even telling the truth. The test is quantification. Genuine efficiency shows up as numbers — revenue growing faster than headcount, cost per claim processed, code shipped per engineer — and shows up in the filings, not just on the call. The narrative version shows up as adjectives: a management citing “AI-driven efficiencies” that cannot say exactly where and exactly how much is suspicious, not making a substantive statement about its operations. The margin line will separate the companies using AI from the companies mentioning it; insist on numbers, not adjectives.

Three — The Follow-Through After the Announcement

The 26.2% headline does lean hard on one supply chain, even if it is awakening the slumbering industrial giant: semiconductors alone are expected to grow around 148% and contribute eleven points of the total, doubling their share of index earnings from 7% to 15% in a single year. Concentration cuts both ways — it built the 26% expectation, and all it takes therefore is deceleration for stock prices to fall into an air pocket.

After all, governments must agree to the projects, land must be purchased, datacenters must be built and equipped, obtain electricity and other utilities, hire staff, and purchase a panoply of equipment and supplies — so is this 26% quarter carried by one industry worth less than a 15% quarter carried by seven? Whether growth broadens is the open question. The manufacturing uptick is indeed one sign that growth is broadening around big new construction, power generation, and the buildout of new facilities and supply capacity.

It’s not as if the rest of the economy is standing still, of course. Many other sectors of the economy are benefiting from rising corporate profits — which find their way into wealth creation nationwide via higher stock prices and higher national income.

Four — Are Order Books, Backlogs, and RPOs Growing?

Order books, backlogs, or remaining performance obligations (RPOs) represent future revenues. When communicating with investors, company managements are incentivized to brag about the revenue a company can see — before it happens. The risk to stock prices is that all this future revenue creates very high expectations, and the market can get “priced for perfection.” Anything smelling like deceleration, delay, or decline can create air pockets as traders react and reset expectations, because it is forward visibility that market participants are really evaluating, and assigning a value to.

Three questions for the semiconductor and AI-infrastructure complex, then. How long — quarters, years, decades? How firm — binding purchase orders, or frameworks dressed up as demand? (An MOU is not a purchase order, by the way.) And, maybe sharpest, given everything we’ve discussed about physical-world bottlenecks: how deliverable — with power, transformers, and specialty materials still the binding constraints, will revenue actually land according to current order book scheduling?

The capital-spending guidance of the hyperscalers — the giant cloud platforms whose budgets are everyone else’s demand — is the other half; note that the check-writers’ own earnings growth is slowing as the build-out’s costs reach their income statements. How far out the order books run, and how binding they are, will matter more than the size of any beat.

This letter is general commentary — the wide-angle view. It is not a portfolio. What we do for the families we work with is the opposite of “wide-angle”: we make portfolios built around one household’s circumstances, taxes, timelines, and appetite for exactly the kind of volatility described above. We keep that roster of clients deliberately small, because that sort of attention doesn’t scale. If you’d like to talk about what it would look like for you, Aubrey Ford will make the time.

Free Cash Flow Falling How Much?

Free cash flow — the cash left over after operating costs and capital spending — is going to fall this season at some of the market’s biggest names. Capital spending hits cash the moment the check clears, while its earnings cost (depreciation) arrives slowly over years, so record earnings per share and shrinking free cash flow can appear in the same report. The question is whether commentary convinces investors that the spending will earn its keep in an appropriate timeframe. Free cash flow is where the AI narrative meets the AI invoice, and we’ve been saying for some time that investors would begin auditing this; as funding the AI buildout gets more complex, we expect the market’s “audit” to get more rigorous.

Oil Prices Represents a Macro Wildcard

All five elements mentioned above play out under one variable no company management can control. Oil sits roughly 30% below its late-April wartime peak despite two weeks of renewed hostilities; the market has moved on from Iran, and the inflation math seems to give its blessing: Goldman Sachs’s models show the war’s price pressure peaked last quarter and fades through year-end absent re-escalation, leaving the Fed on hold. The tail risk is a conflict that neither escalates nor ends. John Bolton argued in the Wall Street Journal this week that Iran really no longer has a government coherent enough to deliver any agreement — its diplomats cannot bind the Revolutionary Guard (of which there are certainly many factions), which kept firing while they talked. A fragmented adversary cannot make peace, and a long simmer keeps a floor under oil.

We should note that even $100 crude adds only a few hundredths of a percent a month to core inflation — soothing arithmetic, but worse psychologically perhaps: after four years of supply shocks, the next might weigh on the Fed’s nerve more than its models.

And we should note also that apart from the price of oil, there are many countries around the world, and especially in Asia, for whom the price of natural gas is an existential concern; investors should bear this calculus in mind as they monitor the global effects of events in the Middle East.

Sober Optimism Warranted

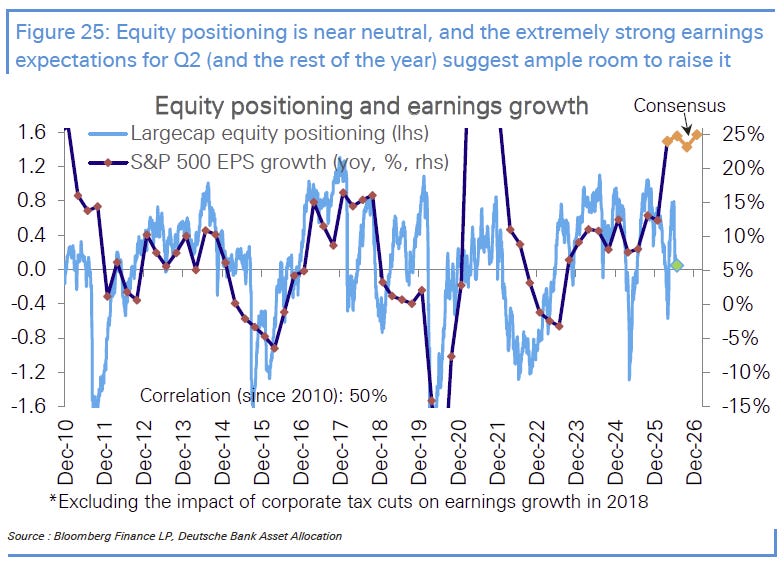

Earnings seasons lift the index about three times in four; positioning sits near neutral, below what earnings this strong usually command; and Deutsche Bank’s model and FactSet’s arithmetic both point to a final growth number near 29%, the best since 2021. Bear markets are born from earnings contractions — many have been caused by those events — but nothing here suggests one. Our posture is still “long America, attentive to the tape”: conviction in the industrial build-out, discipline on the prices we pay to own it, constant attentiveness to find its lesser-known corners.

We also see opportunity in other sectors of the global markets. Japan continues to legislate corporate behavior to make their markets more attractive to foreigners. India is coming into its own as a hub for AI and for technology manufacturing. Latin America is blessed with many important raw materials and it looks as if Marxist-inspired governments in the continent are being replaced with more business-friendly ones.

Thanks for listening; we welcome your calls and questions.

General Disclosures About This Newsletter

The publisher of this newsletter is Guild Investment Management, Inc. (GIM or Guild), an investment advisor registered with the Securities and Exchange Commission. GIM manages the accounts of high net worth individuals, trusts and estates, pension and profit sharing plans, and corporations, among other clients.

Your receipt of this newsletter does not create a personal investment advisory relationship with GIM although some recipients may also be advisory clients of GIM. GIM has written investment advisory agreements with all its personal advisory clients, which sets forth the nature of that relationship.

The newsletter makes general observations about markets and business and financial trends and may provide advice about specific companies and specific investments. It does not give personal investment advice tailored to the needs, objectives, and circumstances of individual readers. Whether investment ideas and recommendations are suitable for individual readers depends substantially on the personal and financial situation of that reader, which GIM, as the publisher of the newsletter, makes no effort to investigate.

GIM attempts to provide accurate content in its newsletters to the extent such content is factual rather than analysis and opinion, but GIM relies primarily on information compiled or reported by third parties and does not generally attempt to independently verify or investigate such information. Moreover, some content and some of the assumptions, formulas, algorithms and other data that affect the content may be inaccurate, outdated, or otherwise flawed. GIM does not guarantee or take responsibility for the accuracy of such information.

Please note that investing in stocks, other securities, and commodities is inherently risky, and you should rely on your personal financial advisors and conduct your own due diligence in connection with any investment decision.

A Special Comment for Guild’s Clients

If you are an investment advisory client of GIM who is receiving this newsletter, please note that the fact that a general recommendation is made of a particular security, commodity, or investment area to its newsletter subscribers does not mean that investment is suitable for you or should be purchased by you. For example, GIM may already have purchased such securities on your behalf or purchased securities in the same industry (and an increase in the position for you may represent too much concentration in one security or industry), or GIM may believe the investment is not suitable for you based on your risk tolerance or other factors. If you have questions about the recommendations in this newsletter in relation to your account at GIM, please contact Tony Danaher, Rudi von Abele, or Aubrey Ford.

Conflicts of Interest

As of the date of this newsletter, GIM’s investment advisory clients or GIM’s principals owned positions in areas that are the subject of current recommendations, commentary, analysis, opinions, or advice, contained in this newsletter.

GIM and its principals have certain conflicts of interest in its relations with its investment advisory clients and its newsletter subscribers resulting from GIM or its principals holding positions for its clients or themselves which are also recommended to its clients. GIM may change the positions of its clients or GIM’s principals may change their positions (increasing, decreasing, and eliminating them) based on GIM’s best judgment at any given time, including the time of publication of the newsletter. Factors that lead GIM to change or eliminate its positions may include general market developments, factors specific to the issuer, or the needs of GIM or its advisory clients. From time to time GIM’s investing goals on behalf of its investment advisory clients or the personal investing goals of GIM’s principals and their risk tolerance may be different from those discussed in the newsletter, and the investment decisions made by GIM for its advisory clients or the investment decisions of its principals may vary from (and may even be contrary to) the advice and recommendations in the newsletter.

In addition, GIM or its principals may reduce or eliminate their positions in an investment that is recommended in the newsletter prior to notifying the newsletter subscribers of such a reduction or elimination. The publication by GIM of a “target price” or “stop loss” for a particular security or other asset does not necessarily represent the price at which GIM intends to sell or will sell any such assets for its advisory clients or the price at which GIM’s principals intend to sell any such assets.

As a consequence of the conflict of interest, GIM’s clients or principals may benefit if newsletter subscribers purchase assets recommended by GIM since it could increase the value of the assets already held by GIM’s investment advisory clients or GIM’s principals. On the other hand, GIM’s principals and clients may suffer a detriment if they seek to acquire additional shares in securities that have been recommended and the price of the securities has increased as a result of purchases by newsletter subscribers.

To help mitigate these conflicts, GIM seeks to avoid recommending the securities of individual companies where GIM or its principals have an ownership position and where the issuer is small or its securities are thinly traded. That way sales by GIM in advance of possible sales by newsletter subscribers would not be likely to cause any significant decrease in the sale price to newsletter subscribers. GIM has a fiduciary relationship with its investment advisory clients and cannot agree on behalf of such clients to refrain from purchases or sales of a security mentioned in the newsletter for a period of time before or after recommendations for purchases or sales are made to its newsletter subscribers.

GIM encourages you to do independent research on the securities or other assets discussed or recommended in the newsletter prior to making any investment decisions and to be especially cautious of investments in small, thinly-traded companies, which are usually the most risky investments that you can make.

Disclaimer of Liability

GIM disclaims any liability for investment decisions based upon recommendations, information, or opinions in its newsletters. GIM is not soliciting you to execute any trade. Nothing contained in GIM’s newsletters is intended to be, nor shall it be construed as an offer to buy or sell securities or to give individual investment advice. The information in the newsletter is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation, or which would subject GIM to any registration requirement within such jurisdiction or country.

COPYRIGHT NOTICE

Guild’s current and past market commentaries are protected by U.S. and international copyright laws. All rights reserved. You must not copy, frame, modify, transmit, further distribute, or use the market commentaries, without the prior written consent of Guild. This email or any download from a secure website is meant for only the intended recipient of the transmission, and may be a communication privileged by law. If you received this email in error, any use, dissemination, distribution, or copying of this email is similarly prohibited. Please notify us immediately of the error by return email and please delete this message from your system. Although this email and any attachments are believed to be free of any virus or other defect that might affect any computer system into which it is received and opened it is the responsibility of the recipient to ensure that it is virus free and no responsibility is accepted by Guild Investment Management for any loss or damage arising in any way from its use.

0 Comments