Some GDP Deceleration, But U.S. Corporates and Consumers Are Still In Good Health

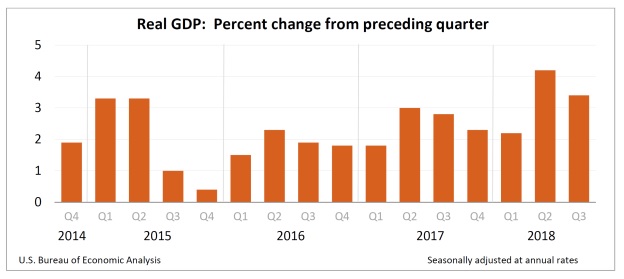

The partial government shutdown in early 2019 has delayed the Commerce Department’s official report on fourth-quarter U.S. GDP growth until February 28. In the absence of official data, polls of economists are providing some picture: about 2.6% annualized real GDP growth in the quarter, bringing full-year 2018 real GDP growth (that is, taking inflation into account) to approximately 3%.

The same polled economists are predicting 1.8% real growth in the first quarter of this year, accelerating to 2.5% in the second quarter. (These estimates seem reasonable to us; of course, the first quarter of the year typically shows a slower growth rate than later quarters.) Economists flag the last quarter’s market turmoil and concerns over global growth (particularly Chinese growth) as the elements responsible for 2019’s deceleration from the 3% pace set during 2018.

To us, the salient point is simply the one noted by an economist who specializes in retail data: “I don’t think we’re seeing anything that we can measure at the macroeconomic level… that would point to any downturn.”

We believe that recent and upcoming stimulus measures from the Chinese government will likely result in a reacceleration of Chinese GDP growth in the second half of 2019. As we often say, stock markets are discounting mechanisms, and we believe Chinese markets are already beginning to reflect an anticipated positive growth inflection.

Investment implications: Although U.S. GDP growth decelerated in the last quarter of 2018, and is likely to continue at a slower pace in the first two quarters of this year, we anticipate that the ongoing health of U.S. corporates’ earnings and U.S. consumers, and the reacceleration of growth in China later in the year, will support markets’ continued progress. Despite the duration of the current expansion — ten years this summer — we do not see signs of imminent recession.