For most of the past decade, “tokenization,” in the minds of most investors, was in the same category as 2017’s meme coins and 2021’s million-dollar cartoon JPEGs of apes — a silly distraction in a then-madly exuberant fringe market, easy to wave away. If that’s still your view, it needs revision.

A quick note: the “tokens” we’re talking about here aren’t the “tokens” used and purchased by AI users — the small chunks of text an AI model reads and generates, usually metered by cost or speed. These are something else: digital records kept on a shared ledger called a “blockchain,” each representing ownership of, or a claim on, a financial or real-world asset. In effect, they are electronic stand-ins that let the underlying asset be bought, sold, and transferred digitally. Thus, tokens record ownership of, or exposure to, an asset as a digital token on a blockchain — a shared electronic ledger that many parties update together, in sync, instead of each keeping a private copy that has to be reconciled afterward.

Strip away the vocabulary and the technology becomes something both boring and critically important: a potentially more efficient (read: fast, accurate, and cheap) transmission and record-keeping financial infrastructure.

The first wave, the “security token offerings” of 2017–2018, mostly failed — there were no agreed standards and nowhere to trade the things (file this under the header of “be a settler, not an explorer”). The market found its footing only when interest rates rose in 2022–2023 and investors wanted somewhere to park cash on-chain; tokenized U.S. Treasury funds (short-term government debt, wrapped in a token) gave them that. Institutional validation arrived in 2024, when BlackRock launched a tokenized fund holding cash and short-term Treasuries, its BUIDL fund (“BlackRock USD Institutional Digital Liquidity Fund”). So did the digital-asset firm Securitize.

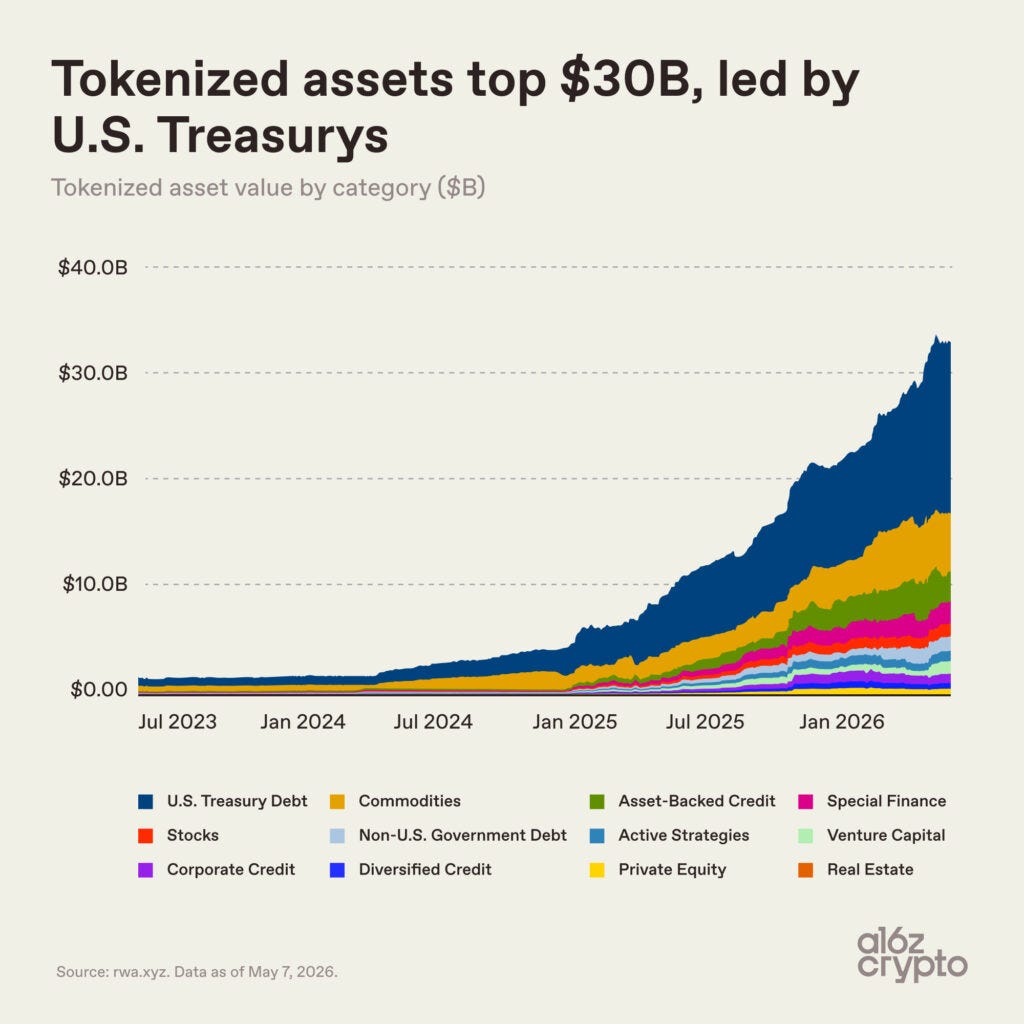

Today the on-chain market for real-world assets, excluding stablecoins (tokens pegged one-to-one to a currency), sits around $31 billion, more than five times its level in early 2025, with tokenized Treasuries the single largest single category at roughly $13-14 billion. Brisk growth — yet still a rounding error against the hundreds of trillions in global assets, and much of it is parked rather than actively traded.

An important distinction: a token can represent genuine ownership — the same economic and voting rights as a traditional share — or merely exposure, a price-tracking IOU issued by a third party with no direct claim on the underlying asset. The two can trade at different prices, particularly when traditional markets are closed, and the exposure version carries the credit risk of whoever issued it. To say that a digital asset is “Tokenized Apple” is not sufficient; investors — and their advisors — have to read and understand the fine print and its implications in various contexts of market and institutional stress.

What are the real risks and “failure modes” of these products and systems? One would hope that the construction of a robust regulatory framework would exhaustively catalog and mitigate those risks — but the history of financial innovation does suggest that there will still be unforeseen “accidents.” (Crypto has of course had plenty of those itself, as it has matured past the libertarian dream and learned the hard lessons already internalized by the regulatory framework that surrounds traditional finance.) We are confident, however, that advancing regulation will gradually make both individual and institutional investors more confident that the advantages of tokenized assets outweigh the risks.

For tokenized assets, as convenient as they might be for end users, the real prize is in the back office. Today’s markets still run on layers of intermediaries, and restricted trading hours; and settlement — the rote business of finalizing a trade, moving cash one way and the asset the other — can take inordinate amounts of time in a technological era where communication is instant. A shared ledger allows nearly instant settlement, where cash and asset change hands at the speed of electrons, around the clock.

This is what BlackRock’s Larry Fink means when he keeps comparing tokenization to the internet around 1996 and describing it as an upgrade to financial plumbing — a bet, as one account framed it, that better rails could turn more people into investors rather than bystanders. Notably, he tells it as a digital-asset story, not a crypto one. The whole field is quietly migrating out of the “crypto” column and into the broader fintech mainstream, with Robinhood, Nasdaq, and the New York Stock Exchange all building tokenized-trading venues.

For investors weighing the second-order effects and looking for a way to capitalize on the trend and avoid potential pitfalls, the most exposed incumbent is the transfer agent — the firm that maintains the official register of who owns a security. A ledger that is the authoritative record threatens to make that function redundant, and regulators have said as much. But the incumbents are not standing still: Securitize and its peers have re-registered as “digital transfer agents,” folding the same record-keeping into the blockchain itself. The lesson is that disintermediation rarely deletes a job; it relocates it.

The infrastructure question is similarly unsettled. Some of these ledgers will be proprietary and private — JPMorgan’s Kinexys network, which already moves billions of dollars a day, is a walled garden. Others are shared and public-but-gated, like the Canton Network that the market’s main clearing utility, the DTCC, has chosen for tokenized assets. The likely winners are less any single chain than the plumbing that lets the chains talk to one another and stay compliant.

We believe great financial advice starts with truly understanding your goals, needs, and circumstances. Schedule a meeting with our Client Relations Director to discover if Guild Investment Management has a solution that will work for you.

Stablecoins won a federal framework in 2025, but broader market-structure rules remain unfinished, and in May 2026 the SEC paused its plan to let firms tokenize stocks without the issuing company’s consent — ostensibly because no one could yet explain how dividends and votes reach a token holder nobody can identify, but we note that the complainants were NASDAQ, NYSE, and CBOE: “interested parties,” one might say. Such resistance is of course inevitable; the transition will be slow, segment by segment, and far less theatrical than the cartoon-ape era that preceded it.

What’s An Investor to Do… A Rundown of Ways to Participate

Tokenization shows up in public equities along a spectrum: a few near-pure-plays that rise and fall with the theme (and carry its full risk), and a set of incumbents where the exposure is real but diluted inside a much larger business.

One caution before the names: almost none of these firms break out a “tokenization” line, so what you can really track is money moving on-chain — assets and volume — not segment revenue. On the pure-play end that activity is compounding fast — the market for tokenized real-world assets is up roughly fivefold in eighteen months — yet the stocks carry risk that has little to do with whether tokenization itself succeeds, since Coinbase’s revenue swings with trading volumes and most of Circle’s is interest earned on the Treasuries behind its stablecoin.

The incumbents are the mirror image: their tokenized segments often grow even faster off a tiny base yet stay almost invisible against the parent — BlackRock’s flagship tokenized fund, at roughly $2.5 billion, is a sliver of one percent of its $14 trillion in assets — so a segment can compound at triple-digit rates for years without ever moving the company’s earnings, which is to say that with the incumbents you are buying the parent’s growth rate, not the theme’s.

The Newer Innovators:

Coinbase (COIN) is the broadest single way to play it. Beyond the exchange, it incubated Base, the low-cost Ethereum “layer-2” network where much tokenized activity and on-chain settlement now live, and it co-founded USDC and supports 60-plus blockchains for settlement. It also acts as primary custodian for roughly 80% of U.S. spot-crypto ETFs — a quiet toll booth — and is in the process of rolling out tokenized equities. The catch: revenue still swings with trading volumes — Q1 2026 net revenue fell to $1.3 billion from $1.9 billion a year earlier.

Circle (CRCL) is the regulated stablecoin layer. It issues USDC, and the majority of its revenue is interest earned on the U.S. Treasuries backing the tokens, which makes it a leveraged bet on both stablecoin adoption and the level of rates — falling interest rates pinch its revenue directly. Note the overlap with Coinbase: both are levered to USDC, so holding both doubles up on the same underlying risk. Since its mid-2025 IPO at $31 the stock has been a rollercoaster — recently around $80, a market cap near $20 billion — and it’s now building its own layer-1 chain (Arc). It owns a tokenized-Treasury product (USYC) which recently overtook BlackRock’s BUIDL as the largest such offering.

Robinhood (HOOD) is the retail-distribution angle — it launched tokenized stock trading for European customers in 2025 and is positioning its app as where ordinary investors first touch tokenized equities.

Galaxy Digital (GLXY) is a diversified digital-asset financial-services firm and, notably, the first US public company to issue tokenized equity on a major public blockchain — a clean, if volatile, thematic proxy.

Bullish (BLSH) is a crypto exchange working to become a digital ledger for traditional capital markets. The company served as its own proof-of-concept by fully tokenizing its 151-million-share cap table on the Solana network (and demonstrating a live wallet-to-wallet transfer at Consensus this year). Enabling this broader strategy is Bullish’s $4.2 billion proposed acquisition of Equiniti, an SEC-registered transfer agent servicing nearly 3,000 public companies and 20 million shareholders; thanks to this acquisition, announced in May, BLSH will bring the functions of share registration and tokenization under the same roof — if the deal is approved by regulators. Because they will own a legacy registry, they will be able safely to write smart contracts that mirror it in real-time within the existing securities-law framework.

The old rails going digital (market infrastructure):

Intercontinental Exchange (ICE) owns the NYSE, which is building a tokenized-securities venue offering 24/7 trading, instant settlement, dollar-sized orders and stablecoin-based funding, combining its Pillar matching engine with blockchain post-trade systems, and has tapped the SEC-registered transfer agent Securitize to help design it. This is the tokenization theme wrapped inside one of the most durable franchises in finance.

Nasdaq (NDAQ) is taking a different tack — an “equity token design” that puts the public issuer at the center of governance, expected to be operational around H1 2027. Like ICE, diluted but high-quality exposure.

Broadridge (BR) is the most direct way to play the recordkeeping shift from the prior piece. Its Distributed Ledger Repo platform already tokenizes more than $365 billion a day, and it has extended its proxy-voting and corporate-actions infrastructure to tokenized shares — the very function transfer agents perform. Rather than being disintermediated, Broadridge is selling the picks and shovels for the transition.

The asset managers putting products on-chain:

BlackRock (BLK) runs BUIDL, until January 2026 the largest tokenized fund (it was overtaken by CRCL’s USYC), and Larry Fink has become the theme’s loudest institutional advocate. Exposure is genuine but a rounding error against nearly $14 trillion in assets — you’re buying the world’s biggest asset manager that just happens to be early in this long-term transition.

Franklin Resources (BEN) was earlier than most: its BENJI token represents an on-chain money-market fund, one of the first registered funds to use public blockchains as a register. Same caveat — small relative to the parent.

Lastly, the custody and servicing (picks and shovels):

BNY (BK) is the world’s largest custodian and already acts as fund administrator and custodian for BlackRock’s BUIDL, broadcasting its fund data on-chain, while exploring tokenized deposits and partnering with Goldman on tokenized money-fund records. State Street (STT) is expanding from servicing crypto ETFs into digital-asset custody, and partnered with Galaxy on a tokenized private-fund. Northern Trust, NTRS, sits in the same camp.

The purest names aren’t (yet) all public. Securitize — the dominant transfer agent for U.S. tokenized funds, including BUIDL — is slated to go public via a SPAC merger (current ticker CEPT, which will become SECZ after the merger is complete) that has been announced but has not yet closed. The DTCC, the clearing utility that picked Canton, is member-owned. And Ondo and Chainlink, central to the plumbing, trade as native tokens on their own networks, not as equities — different instruments, different risks.

In summary, a few years ago, the “blockchain” and “tokenization” were popular drivers of FOMO trading. It did not go away. It may have been replaced in the headlines by more exciting disruptive trends, but make no mistake: it is happening, and will help create… even as it slowly destroys old processes, and maybe a few inflexible legacy companies.

Thanks for listening; we welcome your calls and questions.

General Disclosures About This Newsletter

The publisher of this newsletter is Guild Investment Management, Inc. (GIM or Guild), an investment advisor registered with the Securities and Exchange Commission. GIM manages the accounts of high net worth individuals, trusts and estates, pension and profit sharing plans, and corporations, among other clients.

Your receipt of this newsletter does not create a personal investment advisory relationship with GIM although some recipients may also be advisory clients of GIM. GIM has written investment advisory agreements with all its personal advisory clients, which sets forth the nature of that relationship.

The newsletter makes general observations about markets and business and financial trends and may provide advice about specific companies and specific investments. It does not give personal investment advice tailored to the needs, objectives, and circumstances of individual readers. Whether investment ideas and recommendations are suitable for individual readers depends substantially on the personal and financial situation of that reader, which GIM, as the publisher of the newsletter, makes no effort to investigate.

GIM attempts to provide accurate content in its newsletters to the extent such content is factual rather than analysis and opinion, but GIM relies primarily on information compiled or reported by third parties and does not generally attempt to independently verify or investigate such information. Moreover, some content and some of the assumptions, formulas, algorithms and other data that affect the content may be inaccurate, outdated, or otherwise flawed. GIM does not guarantee or take responsibility for the accuracy of such information.

Please note that investing in stocks, other securities, and commodities is inherently risky, and you should rely on your personal financial advisors and conduct your own due diligence in connection with any investment decision.

A Special Comment for Guild’s Clients

If you are an investment advisory client of GIM who is receiving this newsletter, please note that the fact that a general recommendation is made of a particular security, commodity, or investment area to its newsletter subscribers does not mean that investment is suitable for you or should be purchased by you. For example, GIM may already have purchased such securities on your behalf or purchased securities in the same industry (and an increase in the position for you may represent too much concentration in one security or industry), or GIM may believe the investment is not suitable for you based on your risk tolerance or other factors. If you have questions about the recommendations in this newsletter in relation to your account at GIM, please contact Tony Danaher, Rudi von Abele, or Aubrey Ford.

Conflicts of Interest

As of the date of this newsletter, GIM’s investment advisory clients or GIM’s principals owned positions in areas that are the subject of current recommendations, commentary, analysis, opinions, or advice, contained in this newsletter.

GIM and its principals have certain conflicts of interest in its relations with its investment advisory clients and its newsletter subscribers resulting from GIM or its principals holding positions for its clients or themselves which are also recommended to its clients. GIM may change the positions of its clients or GIM’s principals may change their positions (increasing, decreasing, and eliminating them) based on GIM’s best judgment at any given time, including the time of publication of the newsletter. Factors that lead GIM to change or eliminate its positions may include general market developments, factors specific to the issuer, or the needs of GIM or its advisory clients. From time to time GIM’s investing goals on behalf of its investment advisory clients or the personal investing goals of GIM’s principals and their risk tolerance may be different from those discussed in the newsletter, and the investment decisions made by GIM for its advisory clients or the investment decisions of its principals may vary from (and may even be contrary to) the advice and recommendations in the newsletter.

In addition, GIM or its principals may reduce or eliminate their positions in an investment that is recommended in the newsletter prior to notifying the newsletter subscribers of such a reduction or elimination. The publication by GIM of a “target price” or “stop loss” for a particular security or other asset does not necessarily represent the price at which GIM intends to sell or will sell any such assets for its advisory clients or the price at which GIM’s principals intend to sell any such assets.

As a consequence of the conflict of interest, GIM’s clients or principals may benefit if newsletter subscribers purchase assets recommended by GIM since it could increase the value of the assets already held by GIM’s investment advisory clients or GIM’s principals. On the other hand, GIM’s principals and clients may suffer a detriment if they seek to acquire additional shares in securities that have been recommended and the price of the securities has increased as a result of purchases by newsletter subscribers.

To help mitigate these conflicts, GIM seeks to avoid recommending the securities of individual companies where GIM or its principals have an ownership position and where the issuer is small or its securities are thinly traded. That way sales by GIM in advance of possible sales by newsletter subscribers would not be likely to cause any significant decrease in the sale price to newsletter subscribers. GIM has a fiduciary relationship with its investment advisory clients and cannot agree on behalf of such clients to refrain from purchases or sales of a security mentioned in the newsletter for a period of time before or after recommendations for purchases or sales are made to its newsletter subscribers.

GIM encourages you to do independent research on the securities or other assets discussed or recommended in the newsletter prior to making any investment decisions and to be especially cautious of investments in small, thinly-traded companies, which are usually the most risky investments that you can make.

Disclaimer of Liability

GIM disclaims any liability for investment decisions based upon recommendations, information, or opinions in its newsletters. GIM is not soliciting you to execute any trade. Nothing contained in GIM’s newsletters is intended to be, nor shall it be construed as an offer to buy or sell securities or to give individual investment advice. The information in the newsletter is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation, or which would subject GIM to any registration requirement within such jurisdiction or country.

COPYRIGHT NOTICE

Guild’s current and past market commentaries are protected by U.S. and international copyright laws. All rights reserved. You must not copy, frame, modify, transmit, further distribute, or use the market commentaries, without the prior written consent of Guild. This email or any download from a secure website is meant for only the intended recipient of the transmission, and may be a communication privileged by law. If you received this email in error, any use, dissemination, distribution, or copying of this email is similarly prohibited. Please notify us immediately of the error by return email and please delete this message from your system. Although this email and any attachments are believed to be free of any virus or other defect that might affect any computer system into which it is received and opened it is the responsibility of the recipient to ensure that it is virus free and no responsibility is accepted by Guild Investment Management for any loss or damage arising in any way from its use.