We believe great financial advice starts with truly understanding your goals, needs, and circumstances. Schedule a meeting with our Client Relations Director to discover if Guild Investment Management has a solution that will work for you.

This week we offer some thoughts inspired by our colleague, the redoubtable Larry Jeddeloh of The Institutional Strategist. We are often asked what research we follow and who we read. Larry’s work is very good and is helpful in our process as we pay attention to the macro. In money management, there is a lot of money being managed by people who ignore the macro, as it is full of complex relationships and nuance, and requires study and experience; in short, it is more work. It might not be actionable in your portfolio today, but ignoring the macro seems lazy. Don’t be lazy.

The Shifting Map

U.S. equities remain in a rising trend, though increasingly feeling “tired,” with near-term signals pointing to a modest pullback. With that said, however, the S&P’s late-April breakout has pushed any chatter about a “generational top” much further out, and the main current engines of U.S. outperformance — industrial policy, AI-enabled productivity gains, and capital flowing back home — have, in our view, only just started to do their work.

Three quieter bull markets deserve attention. Energy is one. Defense technology is another, where the action sits with newer entrants rather than the legacy “primes” (that is, the large, established contractors). Mining, especially precious metals, also looks early. None of these carry enough index weight to move the broad market, which is exactly why those who manage their portfolios actively — should care.

A stark imbalance in markets today is the gap between paper and hard assets. U.S. public equity is worth roughly $75 trillion. The front-month value of gold, copper, platinum, palladium, oil, and silver combined sits near $1 trillion. That ratio is near a 55-year low for commodities relative to stocks. The rotation toward real assets — first out of bonds, then out of equities lacking tangible backing — appears to be in early innings, and as the oil story below shows, that rotation can accelerate without much warning.

AI is of course an intimate part of the same story. The buildout is moving from chips to infrastructure: grid, transmission lines, uranium fuel, LNG terminals, turbines, cabling, etc.; power has become the binding constraint. The era of pearl clutching about carbon emissions is fading, giving way to a new era, one where governments and companies around the globe step on the AI accelerator pedal. Sorry, Greta.

Treasuries Get Sold as Oil Prices Bust Budgets

If anyone doubted the hard-asset thesis was already in motion, the past sixty days have offered evidence in real time. Elevated oil prices, driven by disruptions around the Strait of Hormuz, are forcing governments into actions nobody had on the radar two months ago: selling U.S. Treasuries to defend currencies, selling gold to buy oil, cutting taxes to lure foreign capital.

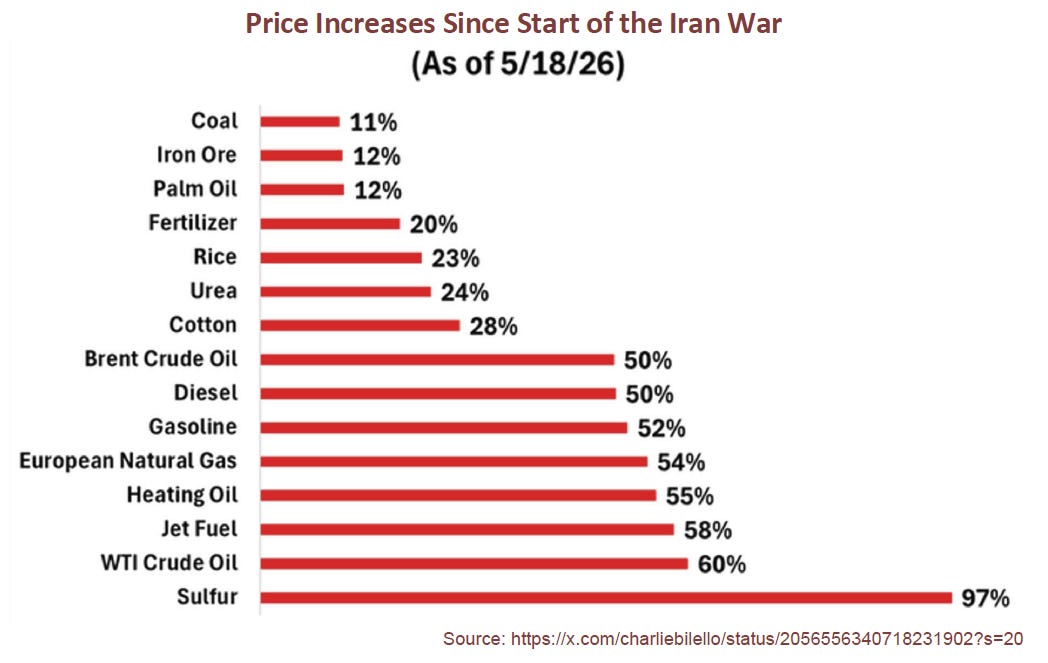

Since the Iran war began, price moves have been dramatic — WTI up roughly 60%, Brent up 50%, gasoline up 52%, jet fuel up 58%. For oil-importing countries, the import bill has ballooned. Local currencies sag, inflation imports itself, and bond yields climb.

We believe great financial advice starts with truly understanding your goals, needs, and circumstances. Schedule a meeting with our Client Relations Director to discover if Guild Investment Management has a solution that will work for you.

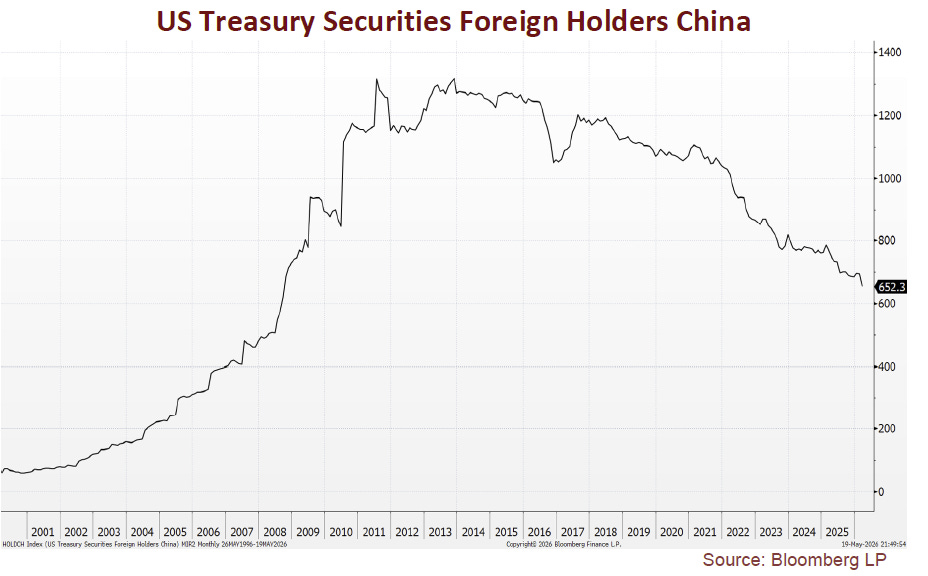

When the U.S. 10-year marches toward 5%, the reflex is to call it a domestic inflation signal, but one major less visible force may be foreign selling — countries unloading Treasuries not because they want to, but because oil and currency stresses leave them little choice. Foreign official holdings have declined, led by Japan trimming $47 billion and China at its lowest level since 2008.

Turkey reported a record $43.4 billion drop in March reserves, much of it from gold sales to finance oil imports, and Turkey is leaning harder on a gold-backed bond program that it originally introduced in 2017. This program is, in plain terms, a gold-collection scheme dressed as a sovereign bond. Turkish households hold an enormous informal hoard — somewhere between 2,200 and 3,500 metric tons by various estimates, much of it jewelry and coins kept at home rather than in banks.

The bonds let citizens turn over that physical metal in exchange for an interest-paying instrument denominated in, and redeemable for, gold. The state gets bullion onto its balance sheet; the depositor gets yield (in lira, or course, pegged to the current gold price), theoretically without giving up gold exposure. Turks have long preferred metal in hand to paper claims on it, of course (as you would too if you lived in a country with Turkey’s track record of currency management) — but lira pressure and the oil import bill have raised the stakes on both sides. This is an interesting attempt of a country with big privately held gold reserves to leverage those — now especially for the purchase of oil.

Turkey’s push indicates the pressure that energy importers are under. For most central banks, U.S. Treasuries are a source of liquidity when conditions demand it, as they do now. We must remember that because of global U.S. dollar hegemony, U.S. long bond yields are, in fact, a global market, and their behavior will reflect it.

U.S. Rates and “Treasury QE”

Memorial Day opens summer driving season at $4.53 per gallon average nationwide, with $5 viewed as the threshold for demand destruction (fellow California residents, we feel your pain). A supply response or de-escalation of Iran war tensions would ease import pressure, stabilize currencies, slow the forced Treasury selling, and let yields drift down — welcome ahead of the midterms.

If neither materializes, the Treasury’s toolkit comes off the shelf: shorter-maturity debt issuance (which reduces the duration risk the market has to absorb), more aggressive buybacks that swap older bonds for fresh paper, and, ultimately, jawboning the Federal Reserve toward long-end purchases. If the Treasury’s actions succeed in reducing bond volatility, that’s a significant overall liquidity booster — as less bond volatility means more collateral value in the system.

Worth noting: some observers now argue that the Treasury has quietly become a more important driver of day-to-day financial conditions than the Fed itself, with “Treasury QE” — the liquidity effect of skewing issuance short and running active buybacks — projected to deliver on the order of $1.3 trillion of duration relief in 2026, comfortably more than anything the Fed is likely to do over the same period. That may overstate the case; the Fed does remain the “lender of last resort,” and the FOMC still matters. Still, investors long trained to watch the Fed exclusively may want to start checking in on Treasury issuance and announcements with similar attention.

Conclusion

The pattern running through these stories may be the early-cycle behavior of a world tilting less towards paper and more towards things. None of this argues at all against equities so much as it argues for particular kinds of equities that have perhaps, in recent years, faded too much from investors’ attention and from visible presence in the market-cap weighted indexes. It argues for renewed attention to companies that own, produce, refine, or build the physical economy: energy, mining, the grid, the infrastructure layer beneath AI, the newer entrants in defense — without neglecting the attention that is due also to the world of AI-driven businesses that will emerge as this technology develops and matures.

Thanks for listening; we welcome your calls and questions.

General Disclosures About This Newsletter

The publisher of this newsletter is Guild Investment Management, Inc. (GIM or Guild), an investment advisor registered with the Securities and Exchange Commission. GIM manages the accounts of high net worth individuals, trusts and estates, pension and profit sharing plans, and corporations, among other clients.

Your receipt of this newsletter does not create a personal investment advisory relationship with GIM although some recipients may also be advisory clients of GIM. GIM has written investment advisory agreements with all its personal advisory clients, which sets forth the nature of that relationship.

The newsletter makes general observations about markets and business and financial trends and may provide advice about specific companies and specific investments. It does not give personal investment advice tailored to the needs, objectives, and circumstances of individual readers. Whether investment ideas and recommendations are suitable for individual readers depends substantially on the personal and financial situation of that reader, which GIM, as the publisher of the newsletter, makes no effort to investigate.

GIM attempts to provide accurate content in its newsletters to the extent such content is factual rather than analysis and opinion, but GIM relies primarily on information compiled or reported by third parties and does not generally attempt to independently verify or investigate such information. Moreover, some content and some of the assumptions, formulas, algorithms and other data that affect the content may be inaccurate, outdated, or otherwise flawed. GIM does not guarantee or take responsibility for the accuracy of such information.

Please note that investing in stocks, other securities, and commodities is inherently risky, and you should rely on your personal financial advisors and conduct your own due diligence in connection with any investment decision.

A Special Comment for Guild’s Clients

If you are an investment advisory client of GIM who is receiving this newsletter, please note that the fact that a general recommendation is made of a particular security, commodity, or investment area to its newsletter subscribers does not mean that investment is suitable for you or should be purchased by you. For example, GIM may already have purchased such securities on your behalf or purchased securities in the same industry (and an increase in the position for you may represent too much concentration in one security or industry), or GIM may believe the investment is not suitable for you based on your risk tolerance or other factors. If you have questions about the recommendations in this newsletter in relation to your account at GIM, please contact Tony Danaher, Rudi von Abele, or Aubrey Ford.

Conflicts of Interest

As of the date of this newsletter, GIM’s investment advisory clients or GIM’s principals owned positions in areas that are the subject of current recommendations, commentary, analysis, opinions, or advice, contained in this newsletter.

GIM and its principals have certain conflicts of interest in its relations with its investment advisory clients and its newsletter subscribers resulting from GIM or its principals holding positions for its clients or themselves which are also recommended to its clients. GIM may change the positions of its clients or GIM’s principals may change their positions (increasing, decreasing, and eliminating them) based on GIM’s best judgment at any given time, including the time of publication of the newsletter. Factors that lead GIM to change or eliminate its positions may include general market developments, factors specific to the issuer, or the needs of GIM or its advisory clients. From time to time GIM’s investing goals on behalf of its investment advisory clients or the personal investing goals of GIM’s principals and their risk tolerance may be different from those discussed in the newsletter, and the investment decisions made by GIM for its advisory clients or the investment decisions of its principals may vary from (and may even be contrary to) the advice and recommendations in the newsletter.

In addition, GIM or its principals may reduce or eliminate their positions in an investment that is recommended in the newsletter prior to notifying the newsletter subscribers of such a reduction or elimination. The publication by GIM of a “target price” or “stop loss” for a particular security or other asset does not necessarily represent the price at which GIM intends to sell or will sell any such assets for its advisory clients or the price at which GIM’s principals intend to sell any such assets.

As a consequence of the conflict of interest, GIM’s clients or principals may benefit if newsletter subscribers purchase assets recommended by GIM since it could increase the value of the assets already held by GIM’s investment advisory clients or GIM’s principals. On the other hand, GIM’s principals and clients may suffer a detriment if they seek to acquire additional shares in securities that have been recommended and the price of the securities has increased as a result of purchases by newsletter subscribers.

To help mitigate these conflicts, GIM seeks to avoid recommending the securities of individual companies where GIM or its principals have an ownership position and where the issuer is small or its securities are thinly traded. That way sales by GIM in advance of possible sales by newsletter subscribers would not be likely to cause any significant decrease in the sale price to newsletter subscribers. GIM has a fiduciary relationship with its investment advisory clients and cannot agree on behalf of such clients to refrain from purchases or sales of a security mentioned in the newsletter for a period of time before or after recommendations for purchases or sales are made to its newsletter subscribers.

GIM encourages you to do independent research on the securities or other assets discussed or recommended in the newsletter prior to making any investment decisions and to be especially cautious of investments in small, thinly-traded companies, which are usually the most risky investments that you can make.

Disclaimer of Liability

GIM disclaims any liability for investment decisions based upon recommendations, information, or opinions in its newsletters. GIM is not soliciting you to execute any trade. Nothing contained in GIM’s newsletters is intended to be, nor shall it be construed as an offer to buy or sell securities or to give individual investment advice. The information in the newsletter is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation, or which would subject GIM to any registration requirement within such jurisdiction or country.

COPYRIGHT NOTICE

Guild’s current and past market commentaries are protected by U.S. and international copyright laws. All rights reserved. You must not copy, frame, modify, transmit, further distribute, or use the market commentaries, without the prior written consent of Guild. This email or any download from a secure website is meant for only the intended recipient of the transmission, and may be a communication privileged by law. If you received this email in error, any use, dissemination, distribution, or copying of this email is similarly prohibited. Please notify us immediately of the error by return email and please delete this message from your system. Although this email and any attachments are believed to be free of any virus or other defect that might affect any computer system into which it is received and opened it is the responsibility of the recipient to ensure that it is virus free and no responsibility is accepted by Guild Investment Management for any loss or damage arising in any way from its use.