This Friday, June 12, SpaceX — now enlarged by the recent merger with Elon Musk’s xAI and the X platform — begins trading on the Nasdaq under the ticker SPCX. At the indicated initial pricing of $135 per share, the offering raises roughly $75 billion and implies a market value near $1.75 trillion. The raise is a record several times over — the previous largest, Saudi Aramco’s in 2019, brought in roughly a third as much — and the valuation narrowly eclipses Aramco’s own debut.

An aside on the week’s market weather, because this IPO is already moving prices. Last week the Nasdaq-100 fell more than 4% in a single session, and as of this writing sits some 7.2% beneath its recent all-time high. The first-order explanation circulating among strategists is simple displacement: would-be SpaceX buyers need cash, and one bank estimates $50 billion or so of other stocks may be sold to make room. IPO allocations must be paid for in full with settled cash — brokers do not extend margin against new issues — so the most leveraged enthusiasts are precisely the ones who must sell something first. Selling to make room has perhaps begotten selling with no choice in the matter.

On the deal itself, we’ll say what we admire before we say what gives us pause. Several of SpaceX’s core businesses are exemplars of a dynamism reminiscent of 19th and 20th-century industry at its most ambitious. The company delivers roughly 90% of all payload mass launched into orbit worldwide, and operates a satellite-broadband constellation (Starlink) that no competitor can easily replicate and has grown revenue from $10.4 billion to $18.7 billion in two years. No one could cogently maintain that SpaceX is a bad business. Our concern is rather with a different question: in this transaction, what role has been provided for the individual investor? Reading the prospectus, we keep arriving at the same uncomfortable answer. We like to say, “Don’t be someone else’s exit liquidity” — and this offering is a request that you volunteer.

To be sure, the loose version of that charge is false. No insider sells a single share on Friday; the offering is “all-primary,” meaning every dollar raised goes to the company (and the investment banks), and existing holders are contractually locked up for weeks at least. What the prospectus does contain is a programmatic exit calendar. Lockup releases begin around late August. A first tranche — 20% of each locked holder’s eligible shares, roughly 900 million in all, plus an additional 10% if the stock holds 30% above the IPO price — unlocks within days of the first public earnings report, with smaller tranches following at regular intervals through the fall. The single biggest wave, up to 1.3 billion shares — roughly 28% of the shares subject to the staggered schedule, or about a tenth of the company — arrives near the November earnings release, and the remainder comes free at the 180-day mark in early December. All told, the tradable float swells from about 4% of shares outstanding at the open to roughly 40% by year-end. This is to say that the people who know the company best have scheduled their opportunity to sell.

The extent to which the offering is being made through retail channels is unusual and telling. Shares are being distributed to individuals through Schwab, Fidelity, Robinhood, SoFi, and E*TRADE, with as much as 30% of the offering earmarked for retail — several times the 5–10% typical of large deals — and a separate directed-share program reserving up to 5% more for certain employees and associates. Further, index rule changes — Nasdaq’s new fast-entry pathway chief among them — could compel passive funds to buy an estimated $22 to $27 billion of SPCX within days or weeks of listing, precisely while the float is at its thinnest. Notably, the largest passive pool of all will be absent: S&P Dow Jones declined last week to bend its rules, and its profitability requirement keeps SPCX out of the S&P 500 until mid-2027 at the earliest — so no S&P 500 bid will be waiting when the lockup supply arrives this autumn; the Nasdaq-100 and Russell buying will have come and gone by midsummer.

The float at the open is thin — only the 555.6 million new shares trade freely (perhaps 639 million if the underwriters exercise their option to sell an additional block), with roughly 60% of the company locked for over a year. Engineered scarcity plus engineered demand is a fine recipe for a strong debut.

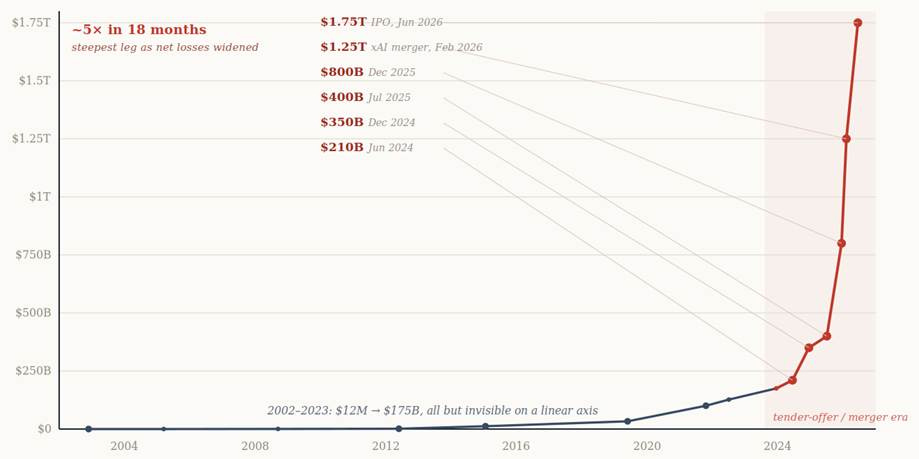

Now, on to the deal price itself. SpaceX’s own risk factors enumerated in the deal prospectus concede that the price “may not reflect our actual operating performance.” The chart below shows a valuation that crawled along the floor for two decades — $12 million in 2002, still $175 billion in 2023 — and then went nearly vertical: $350 billion in the December 2024 tender, $800 billion a year later, and $1.75 trillion today, a fivefold move in eighteen months of tender offers and the xAI merger.

We believe great financial advice starts with truly understanding your goals, needs, and circumstances. Schedule a meeting with our Client Relations Director to discover if Guild Investment Management has a solution that will work for you.

The consolidated company is really three businesses in very different seasons of growth. Starlink — the “Connectivity” segment — is the cash engine: $11.4 billion of revenue in 2025, up roughly 50% from the prior year, throwing off $4.4 billion in operating income. The legacy launch business, for all its dominance, actually swung to a modest operating loss in 2025 as Starship development spending ramped. And the newly absorbed xAI is the biggest source of red ink: a $6.4 billion segment operating loss last year, alongside $12.7 billion in capital spending — roughly triple what either other segment invested. A little more in the weeds, Starlink’s average revenue per user (ARPU) — the monthly amount a typical subscriber pays — has slid from $99 in 2023 to $66 in the most recent quarter as growth tilts toward lower-priced international markets. In other words, the one division that justifies the valuation is getting bigger and less lucrative per customer at the same time: a deliberate trade of price for reach, to be sure, and so far a profitable one, but potential investors should note the phase of expansion this business is in and the relevant dynamics and challenges.

Of course, insiders have in fact been selling all along — privately. As recently as December, SpaceX ran a tender letting eligible holders cash out at a price that, adjusted for this spring’s five-for-one stock split, works out to about $84 per share. The last time the people closest to this company actually sold, six months ago, they accepted nearly 40% less than public retail investors are being “offered” on Friday. Meanwhile, the steepest leg of the chart coincided with a swing from a $791 million profit in 2024 to a $4.9 billion loss in 2025, losses that accelerated to $4.3 billion in the first quarter of 2026 alone. At 94 times 2025 revenue, independent fair-value estimates we have seen run from roughly $780 billion to $1.3 trillion — half to three-quarters of the offer.

For that premium valuation, Spacex’s newest shareholders will have virtually no say in what goes on in the company. A Class A share, meanwhile, carries almost no voting power, where Musk will retain about 82.4%. Even more than in most similar cases, shareholders will be holding a token of price participation, and not of governance.

A brief aside on a deal struck just last week, because it bears on how to read the xAI segment. On June 5, SpaceX disclosed an agreement under which Google will pay it $920 million per month — roughly $29 billion through mid-2029 — for access to about 110,000 GPUs at the xAI data centers in Memphis. This follows a May agreement leasing the entirety of the original Colossus facility to Anthropic for $1.25 billion a month over three years. Bulls will read these as validation, and not without reason: that is something like $75 billion of contracted revenue, signed by sophisticated counterparties, set against a segment that booked $818 million of revenue and a $2.5 billion operating loss in the first quarter. In a compute-starved market, monetizing spare capacity is rational.

But consider what the transaction quietly reveals. Frontier AI labs treat computing power as their scarcest strategic asset; the leading ones spend their energies acquiring every available chip on the theory that more compute becomes a better model becomes a durable franchise. A lab confident in that arithmetic does not rent its GPUs, at landlord margins, to a company its own prospectus names as a competitor in both AI and connectivity. Apparently, then, management’s estimate of the return on training Grok, at the margin, evidently runs below the rent Google is willing to pay.

Take this next part with a grain of salt — it is industry chatter, not anything in a filing — but the talk in data-center circles is that the original Colossus facility was assembled so quickly, from such a mixed fleet of chip generations, that it proved awkward for training xAI’s own frontier models, which decamped to the newer Colossus 2. If true, the leases are less a strategy than a graceful monetization of hardware the company outgrew. Either way, there is a perfectly respectable business in being paid rent — it is the business of CoreWeave and the other “neoclouds,” as the data-center landlords are called — but the market values landlords as infrastructure, at infrastructure multiples. Investors underwriting xAI as a frontier laboratory should notice when it begins behaving like a very large landlord.

And here’s a parting thought about the history of mega-cap tech IPOs. Truist analysis of the past two decades of such IPOs shows them down 9% on average at both the six- and twelve-month marks — with the majority suffering substantial drawdowns in year one; the median peak-to-trough decline across the sample reportedly ran near 54%. Facebook fell 54% from its post-IPO peak and ended its first year down 32% while the broad market rose 10%, before going on to become one of the great compounders of its era. Lyft, Coinbase, Robinhood, and Rivian fell 65%, 55%, 74%, and 67% respectively within twelve months of listing. So even the eventual big winners among the mega-IPOs have offered the patient buyer a materially better price at some point in their first year.

So in the end, the very things that concern us work in a patient investor’s favor. If the ongoing supply wave pressures the price through autumn, better entry points will arrive just when buyers will also have something no one has on Friday: real public quarterly financials, evidence on whether Starlink’s declining revenue per subscriber stabilizes and whether xAI’s losses are showing any positive inflection. If instead the bulls are right, waiting costs a slice of upside in a company they expect to compound for decades — a modest toll. Of course, this conclusion is no secret and it is shared by many analysts, and to the extent the autumn supply wave is widely anticipated, some of its effect will be priced in before it arrives. The asymmetry favors patience, and SpaceX may well prove a magnificent public company. Just be polite and hold the door for someone else go through first.

Thanks for listening; we welcome your calls and questions.

General Disclosures About This Newsletter

The publisher of this newsletter is Guild Investment Management, Inc. (GIM or Guild), an investment advisor registered with the Securities and Exchange Commission. GIM manages the accounts of high net worth individuals, trusts and estates, pension and profit sharing plans, and corporations, among other clients.

Your receipt of this newsletter does not create a personal investment advisory relationship with GIM although some recipients may also be advisory clients of GIM. GIM has written investment advisory agreements with all its personal advisory clients, which sets forth the nature of that relationship.

The newsletter makes general observations about markets and business and financial trends and may provide advice about specific companies and specific investments. It does not give personal investment advice tailored to the needs, objectives, and circumstances of individual readers. Whether investment ideas and recommendations are suitable for individual readers depends substantially on the personal and financial situation of that reader, which GIM, as the publisher of the newsletter, makes no effort to investigate.

GIM attempts to provide accurate content in its newsletters to the extent such content is factual rather than analysis and opinion, but GIM relies primarily on information compiled or reported by third parties and does not generally attempt to independently verify or investigate such information. Moreover, some content and some of the assumptions, formulas, algorithms and other data that affect the content may be inaccurate, outdated, or otherwise flawed. GIM does not guarantee or take responsibility for the accuracy of such information.

Please note that investing in stocks, other securities, and commodities is inherently risky, and you should rely on your personal financial advisors and conduct your own due diligence in connection with any investment decision.

A Special Comment for Guild’s Clients

If you are an investment advisory client of GIM who is receiving this newsletter, please note that the fact that a general recommendation is made of a particular security, commodity, or investment area to its newsletter subscribers does not mean that investment is suitable for you or should be purchased by you. For example, GIM may already have purchased such securities on your behalf or purchased securities in the same industry (and an increase in the position for you may represent too much concentration in one security or industry), or GIM may believe the investment is not suitable for you based on your risk tolerance or other factors. If you have questions about the recommendations in this newsletter in relation to your account at GIM, please contact Tony Danaher, Rudi von Abele, or Aubrey Ford.

Conflicts of Interest

As of the date of this newsletter, GIM’s investment advisory clients or GIM’s principals owned positions in areas that are the subject of current recommendations, commentary, analysis, opinions, or advice, contained in this newsletter.

GIM and its principals have certain conflicts of interest in its relations with its investment advisory clients and its newsletter subscribers resulting from GIM or its principals holding positions for its clients or themselves which are also recommended to its clients. GIM may change the positions of its clients or GIM’s principals may change their positions (increasing, decreasing, and eliminating them) based on GIM’s best judgment at any given time, including the time of publication of the newsletter. Factors that lead GIM to change or eliminate its positions may include general market developments, factors specific to the issuer, or the needs of GIM or its advisory clients. From time to time GIM’s investing goals on behalf of its investment advisory clients or the personal investing goals of GIM’s principals and their risk tolerance may be different from those discussed in the newsletter, and the investment decisions made by GIM for its advisory clients or the investment decisions of its principals may vary from (and may even be contrary to) the advice and recommendations in the newsletter.

In addition, GIM or its principals may reduce or eliminate their positions in an investment that is recommended in the newsletter prior to notifying the newsletter subscribers of such a reduction or elimination. The publication by GIM of a “target price” or “stop loss” for a particular security or other asset does not necessarily represent the price at which GIM intends to sell or will sell any such assets for its advisory clients or the price at which GIM’s principals intend to sell any such assets.

As a consequence of the conflict of interest, GIM’s clients or principals may benefit if newsletter subscribers purchase assets recommended by GIM since it could increase the value of the assets already held by GIM’s investment advisory clients or GIM’s principals. On the other hand, GIM’s principals and clients may suffer a detriment if they seek to acquire additional shares in securities that have been recommended and the price of the securities has increased as a result of purchases by newsletter subscribers.

To help mitigate these conflicts, GIM seeks to avoid recommending the securities of individual companies where GIM or its principals have an ownership position and where the issuer is small or its securities are thinly traded. That way sales by GIM in advance of possible sales by newsletter subscribers would not be likely to cause any significant decrease in the sale price to newsletter subscribers. GIM has a fiduciary relationship with its investment advisory clients and cannot agree on behalf of such clients to refrain from purchases or sales of a security mentioned in the newsletter for a period of time before or after recommendations for purchases or sales are made to its newsletter subscribers.

GIM encourages you to do independent research on the securities or other assets discussed or recommended in the newsletter prior to making any investment decisions and to be especially cautious of investments in small, thinly-traded companies, which are usually the most risky investments that you can make.

Disclaimer of Liability

GIM disclaims any liability for investment decisions based upon recommendations, information, or opinions in its newsletters. GIM is not soliciting you to execute any trade. Nothing contained in GIM’s newsletters is intended to be, nor shall it be construed as an offer to buy or sell securities or to give individual investment advice. The information in the newsletter is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation, or which would subject GIM to any registration requirement within such jurisdiction or country.

COPYRIGHT NOTICE

Guild’s current and past market commentaries are protected by U.S. and international copyright laws. All rights reserved. You must not copy, frame, modify, transmit, further distribute, or use the market commentaries, without the prior written consent of Guild. This email or any download from a secure website is meant for only the intended recipient of the transmission, and may be a communication privileged by law. If you received this email in error, any use, dissemination, distribution, or copying of this email is similarly prohibited. Please notify us immediately of the error by return email and please delete this message from your system. Although this email and any attachments are believed to be free of any virus or other defect that might affect any computer system into which it is received and opened it is the responsibility of the recipient to ensure that it is virus free and no responsibility is accepted by Guild Investment Management for any loss or damage arising in any way from its use.