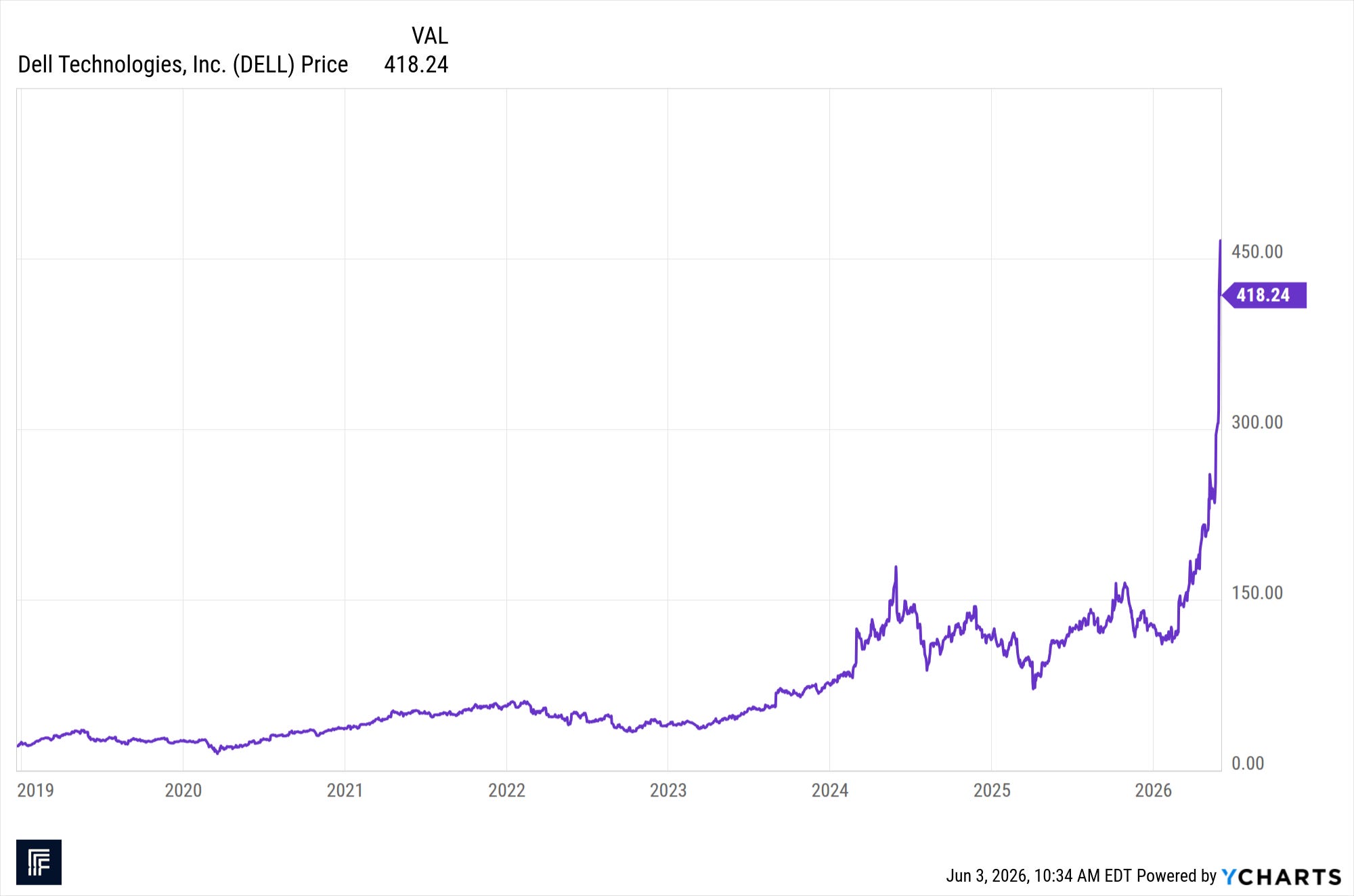

There is a particular kind of chart that tends to make us equal parts pleased and uneasy: the parabola. Lines that bend skyward at an accelerating rate are exhilarating to own, painful to watch from the sidelines, and miserable to time, because the same steepness that rewards you on the way up does nothing to cushion the way down. Dell is this quarter’s exhibit — a stock we still own for our clients, though we have been trimming during its rise.

A company that spent a decade being filed under “old PC name” reported a blowout AI-server quarter in late May and ran from the low $200s to above $400 in a matter of weeks — a roughly 290% gain on the year. Now, contrary to the worst cases of the dotcom era, in this case, the business is real; the AI-server backlog is real; the order book is real. But does the price already assume a version of the future that has to arrive precisely on schedule in order to maintain the momentum?

That brings us to another set of numbers that crossed our desk: a recent analysis of the announced data center pipeline that was a usefully sobering take on the AI build-out in months. (We don’t want to be so sober that we miss the party, but we also don’t want to lose our wits: there’s a happy medium.) Its central finding: of the 100-plus gigawatts of capacity announced for delivery through 2030, as much as 60% may be “at risk” — meaning, unlikely to materialize on the announced timeline (or, potentially, at all). Of roughly 102 GW of announced capacity, only about 40 GW clears a credible project-readiness screen.

Which number didn’t move? In the past quarter, the announced pipeline grew by more than 100 GW, but operational capacity — gigawatts actually plugged in and running — grew by zero. The headline writes itself: a hundred gigawatts of new announcements, not one new gigawatt on the grid.

Even with Abundant Liquidity, Physical Constraints > Financial Constraints

We can pretend to assume that capital solves everything. Perhaps it does — eventually. The bottlenecks are stubbornly material and cannot be instantly conjured away by capital: power procurement (grid access and multi-year equipment lead times), permitting and community opposition, the absence of signed offtake contracts, thin coordination with utilities. Money is abundant; transformers, interconnection queues, and permitted megawatts are not. You cannot wire a substation faster by raising another round.

The timeline, in other words, is elongating rather than compressing. Roughly 70% of the announced pipeline is in the 2027–2028 window, but many of those projects may carry sub-40% odds of arriving on time. The first true megaprojects are already slipping — delays jumped more than fourfold in a single quarter, led by an 11 GW Texas campus now pushed out. The demand may well be durable, but the delivery is physically constrained, and those are very different statements with very different investment implications — particularly in a universe such as ours where valuations are based on the anticipation and modeling of future events.

None of this says the AI thesis is wrong. It says the build-out will be lumpier, slower, and more concentrated among operators who can actually execute — the hyperscalers with the balance sheets, the utility relationships, and increasingly, with their own power.

The majors spent the quarter quietly turning into power companies: Meta expanded a 6.6 GW nuclear portfolio while funding seven new gas-fired plants; Microsoft went off-grid for the first time with a 1.35 GW natural-gas microgrid; Oracle contracted 1.2 GW of Bloom Energy fuel cells and laid out plans for a campus powered by three small modular reactors — the compact, factory-built nuclear units that several operators are betting on for carbon-free baseload. Google signed clean-energy and demand-response deals; Amazon committed $25 billion to data centers across Mississippi and another $15 billion in northern Indiana — and, tellingly, agreed in both cases to cover the full cost of the new power and grid infrastructure those campuses require rather than wait in the utility interconnection queue, even pledging to fund more generation in Indiana than the facilities themselves will consume. A slower, more disciplined cycle is probably healthier than a speculative one, but this just isn’t the kind of cycle priced into the most parabolic names.

We believe great financial advice starts with truly understanding your goals, needs, and circumstances. Schedule a meeting with our Client Relations Director to discover if Guild Investment Management has a solution that will work for you.

What Makes Sentiment Sour?

Good stock markets don’t usually wait for bad news to turn; they often turn on the mere possibility of potential disappointment. It won’t be the realization that the destination is not real, it will be the realization that the “timing” to the destination is being stretched. The dangerous gap is not “will AI demand exist” but “will it exist this quarter, at this run-rate, to justify this multiple.” Expectations of imminence — the embedded assumption that capacity announced today is revenue tomorrow — leaves tech stocks vulnerable to a repricing event. When 60% of a pipeline is on paper and the market has paid for it as though it were poured in concrete, the eventual reconciliation is going to be uncomfortable.

Our strategy follows from that. We’ve been trimming the names that have gone vertical, not because we doubt the secular story, but because the math of a parabola is unforgiving and the risk/reward at these levels is getting asymmetric. And we are looking the other way down the value chain — toward the companies that relieve the bottlenecks rather than the ones whose valuations assume the bottlenecks don’t exist. If the binding constraint is power and interconnection, the durable beneficiaries are likelier to be the grid-equipment makers, the independent power producers, the nuclear and fuel-cell suppliers, and the utilities with data centers queued at their gates.

Beyond energy, the bottlenecks can get strangely specific. One fund manager’s research we have seen makes the case at the level of individual components — and the examples are unglamorous. Consider the multi-layer ceramic capacitor, or MLCC: a tiny passive component, produced by the billions, whose job is to store and release small bursts of electrical charge and so smooth out the power delivered to a chip. A smartphone uses perhaps a thousand of them; a single high-end AI server rack may need more than a million. On that manager’s estimates, AI could consume 10–15% of the entire global MLCC supply within eighteen months, up from roughly 2% today — a step-change that the handful of dominant Japanese and Taiwanese manufacturers are not obviously racing to meet.

Or consider glass. The fiberglass and specialized low-loss glass used in circuit boards and advanced chip packaging has, on the same account, gone from a couple of months of inventory to effectively none, with manufacturers pushing through repeated price increases. The pattern repeats across memory chips, copper foil, the equipment used to make semiconductors, and — more speculatively — ordinary CPUs, which may be needed in far greater numbers as the industry shifts from training models to running them (including locally-running AI agents).

When everyone is staring at the obvious hardware winners, some more interesting risk-reward may sit a few layers down the supply chain, in the boring little parts nobody talks about until they run out.

Speaking of Running Out…

Back to the energy theme: a small but striking dispatch this week. Speaking at a summit in Regina, India’s High Commissioner to Canada signaled that New Delhi would be prepared to buy all the uranium Cameco could supply, and was eyeing investment in Canadian mining projects besides, as it expands its nuclear fleet. Cameco shares rose more than 6% on the remark.

Take it with the appropriate grain of salt — “we’ll take everything you’ve got” is the language of an opening position at a conference, not a signed supply agreement, and one diplomat’s enthusiasm is not a contract. But the direction is the point, and it rhymes with everything above. The AI build-out’s most obvious and painful constraint is electricity, the cleanest scalable baseload answer is increasingly nuclear, and nuclear runs on a fuel with a supply chain that takes the better part of a decade to expand. When sovereign buyers start talking about cornering a producer’s entire output, it tells you the demand for power is being taken seriously at the highest levels — and that the interesting opportunities may sit upstream of the data centers entirely, in the business of digging up and enriching the fuel.

The summary? At this stage, for the investment portfolios we manage, our preference is to find more of the pick-and-shovel relievers of the genuine bottlenecks, than the parabolas that assume there aren’t any.

Thanks for listening; we welcome your calls and questions.

General Disclosures About This Newsletter

The publisher of this newsletter is Guild Investment Management, Inc. (GIM or Guild), an investment advisor registered with the Securities and Exchange Commission. GIM manages the accounts of high net worth individuals, trusts and estates, pension and profit sharing plans, and corporations, among other clients.

Your receipt of this newsletter does not create a personal investment advisory relationship with GIM although some recipients may also be advisory clients of GIM. GIM has written investment advisory agreements with all its personal advisory clients, which sets forth the nature of that relationship.

The newsletter makes general observations about markets and business and financial trends and may provide advice about specific companies and specific investments. It does not give personal investment advice tailored to the needs, objectives, and circumstances of individual readers. Whether investment ideas and recommendations are suitable for individual readers depends substantially on the personal and financial situation of that reader, which GIM, as the publisher of the newsletter, makes no effort to investigate.

GIM attempts to provide accurate content in its newsletters to the extent such content is factual rather than analysis and opinion, but GIM relies primarily on information compiled or reported by third parties and does not generally attempt to independently verify or investigate such information. Moreover, some content and some of the assumptions, formulas, algorithms and other data that affect the content may be inaccurate, outdated, or otherwise flawed. GIM does not guarantee or take responsibility for the accuracy of such information.

Please note that investing in stocks, other securities, and commodities is inherently risky, and you should rely on your personal financial advisors and conduct your own due diligence in connection with any investment decision.

A Special Comment for Guild’s Clients

If you are an investment advisory client of GIM who is receiving this newsletter, please note that the fact that a general recommendation is made of a particular security, commodity, or investment area to its newsletter subscribers does not mean that investment is suitable for you or should be purchased by you. For example, GIM may already have purchased such securities on your behalf or purchased securities in the same industry (and an increase in the position for you may represent too much concentration in one security or industry), or GIM may believe the investment is not suitable for you based on your risk tolerance or other factors. If you have questions about the recommendations in this newsletter in relation to your account at GIM, please contact Tony Danaher, Rudi von Abele, or Aubrey Ford.

Conflicts of Interest

As of the date of this newsletter, GIM’s investment advisory clients or GIM’s principals owned positions in areas that are the subject of current recommendations, commentary, analysis, opinions, or advice, contained in this newsletter.

GIM and its principals have certain conflicts of interest in its relations with its investment advisory clients and its newsletter subscribers resulting from GIM or its principals holding positions for its clients or themselves which are also recommended to its clients. GIM may change the positions of its clients or GIM’s principals may change their positions (increasing, decreasing, and eliminating them) based on GIM’s best judgment at any given time, including the time of publication of the newsletter. Factors that lead GIM to change or eliminate its positions may include general market developments, factors specific to the issuer, or the needs of GIM or its advisory clients. From time to time GIM’s investing goals on behalf of its investment advisory clients or the personal investing goals of GIM’s principals and their risk tolerance may be different from those discussed in the newsletter, and the investment decisions made by GIM for its advisory clients or the investment decisions of its principals may vary from (and may even be contrary to) the advice and recommendations in the newsletter.

In addition, GIM or its principals may reduce or eliminate their positions in an investment that is recommended in the newsletter prior to notifying the newsletter subscribers of such a reduction or elimination. The publication by GIM of a “target price” or “stop loss” for a particular security or other asset does not necessarily represent the price at which GIM intends to sell or will sell any such assets for its advisory clients or the price at which GIM’s principals intend to sell any such assets.

As a consequence of the conflict of interest, GIM’s clients or principals may benefit if newsletter subscribers purchase assets recommended by GIM since it could increase the value of the assets already held by GIM’s investment advisory clients or GIM’s principals. On the other hand, GIM’s principals and clients may suffer a detriment if they seek to acquire additional shares in securities that have been recommended and the price of the securities has increased as a result of purchases by newsletter subscribers.

To help mitigate these conflicts, GIM seeks to avoid recommending the securities of individual companies where GIM or its principals have an ownership position and where the issuer is small or its securities are thinly traded. That way sales by GIM in advance of possible sales by newsletter subscribers would not be likely to cause any significant decrease in the sale price to newsletter subscribers. GIM has a fiduciary relationship with its investment advisory clients and cannot agree on behalf of such clients to refrain from purchases or sales of a security mentioned in the newsletter for a period of time before or after recommendations for purchases or sales are made to its newsletter subscribers.

GIM encourages you to do independent research on the securities or other assets discussed or recommended in the newsletter prior to making any investment decisions and to be especially cautious of investments in small, thinly-traded companies, which are usually the most risky investments that you can make.

Disclaimer of Liability

GIM disclaims any liability for investment decisions based upon recommendations, information, or opinions in its newsletters. GIM is not soliciting you to execute any trade. Nothing contained in GIM’s newsletters is intended to be, nor shall it be construed as an offer to buy or sell securities or to give individual investment advice. The information in the newsletter is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation, or which would subject GIM to any registration requirement within such jurisdiction or country.

COPYRIGHT NOTICE

Guild’s current and past market commentaries are protected by U.S. and international copyright laws. All rights reserved. You must not copy, frame, modify, transmit, further distribute, or use the market commentaries, without the prior written consent of Guild. This email or any download from a secure website is meant for only the intended recipient of the transmission, and may be a communication privileged by law. If you received this email in error, any use, dissemination, distribution, or copying of this email is similarly prohibited. Please notify us immediately of the error by return email and please delete this message from your system. Although this email and any attachments are believed to be free of any virus or other defect that might affect any computer system into which it is received and opened it is the responsibility of the recipient to ensure that it is virus free and no responsibility is accepted by Guild Investment Management for any loss or damage arising in any way from its use.