If you strip the AI rally down to what the money is actually buying, you finally find transformers, high-voltage switchgear, copper, industrial-scale cooling, gas turbines, and data centers whose power draw rivals that of a midsize country — a build-out that Goldman Sachs estimates at roughly $7.6 trillion between 2026 and 2031. Market commentary may call this “technology,” but the invoices read “heavy industry.”

The familiar worry about AI is a demand question — “will adoption and revenue ever justify the spending?” Perhaps a more interesting uncertainty is on the supply side: whether the physical build can actually be delivered, and, most interesting for investors, who will get paid to deliver it. Goldman’s own framing splits that $7.6 trillion into compute (about $5.1 trillion), the data centers themselves (roughly $2.1 trillion), and power (a smaller but fast-growing $0.4 trillion) — and notes that a next-generation AI facility now costs over $20 million per megawatt to build, up from around $10 million during the cloud buildout.

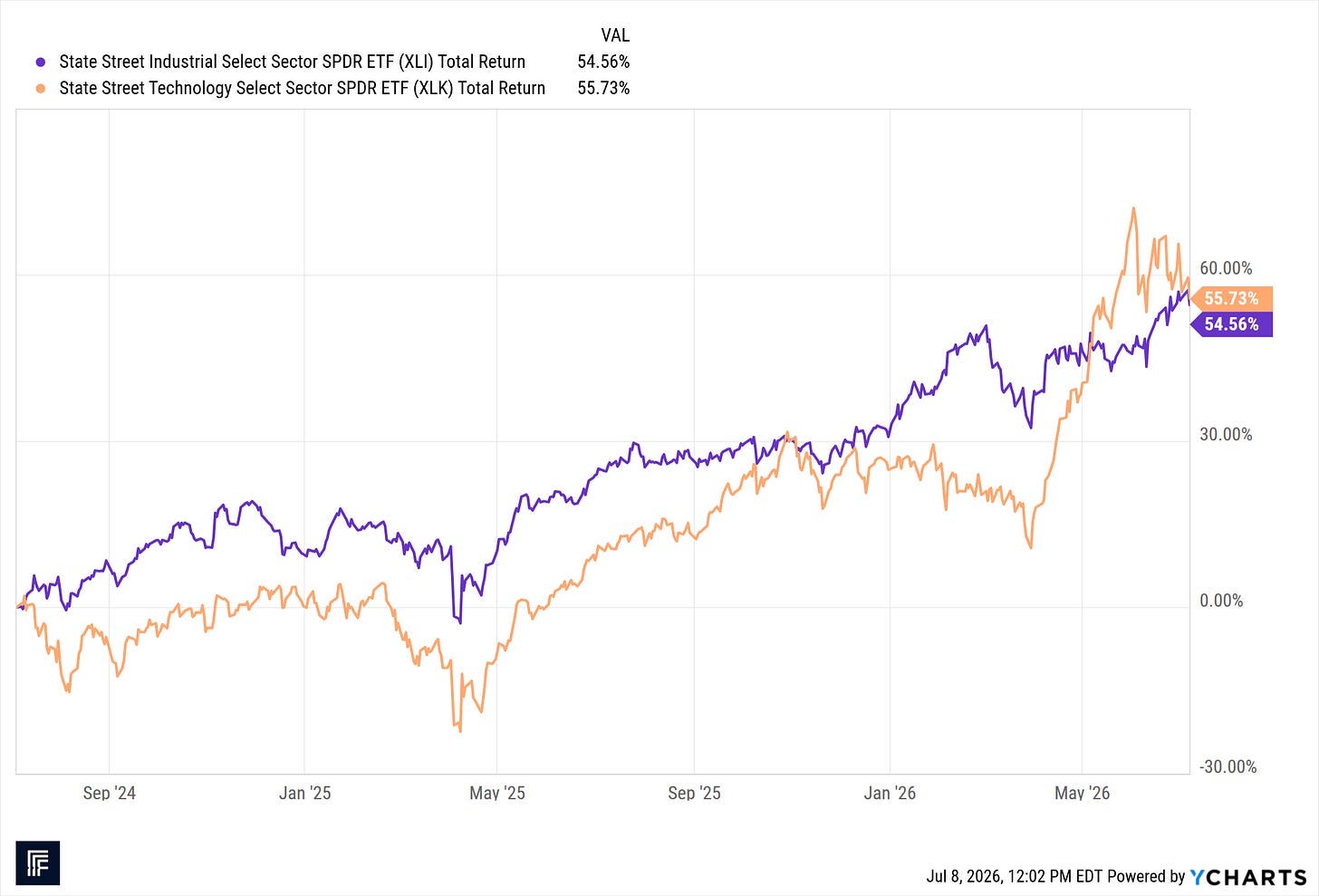

Chips get the headlines, but the copper, the capacitors, the cooling, and the concrete get the checks. The AI build-out is an industrial event misfiled under “technology,” and there will be downstream consequences (positive and negative) visible throughout the industrial sector.

We’ve argued for most of this year that we see the more durable investment trend for AI lies behind the chips — in the power, components, and materials that relieve the bottlenecks — rather than the cyclical hardware names creating the bottlenecks (several of whose stock prices went parabolic). The binding constraint has moved from compute to the physical inputs around it (as we can see from the intelligent selling and leasing of excess compute in various hyperscaler deals) — interconnection queues, transformers, switchgear, turbines, and cooling, all with lead times measured in years. A shortage today is not a moat tomorrow, to be sure; but the direction of travel is unambiguous: the AI story is dragging a very old-economy supply chain forward with it.

Further, the industrial pull is not only coming from AI. On last week’s call we walked through the tailwinds behind the U.S. economy and a reindustrialization that is now backed by policy rather than hope — reshoring, security-as-industrial-policy, and a manufacturing base that Washington has decided, on a bipartisan basis, it wants to be more at home. With the June payroll print soft enough (+57,000, with the two prior months revised down) to keep the Federal Reserve from over-tightening, and industrial raw-material prices — steel and the like — breaking out over the past six months even as oil and precious metals fell, Mizuho calls industrials “a perfect rotation candidate from the crowded AI trade.” Add the reconstruction and fresh natural-gas capacity following the as-yet unresolved disruption in the Gulf, and the non-residential construction boom stops looking like a single-story building. For the first time in a generation, industrial demand has a policy tailwind behind it, rather than merely a cyclical one.

This letter is general commentary — the wide-angle view. It is not a portfolio. What we do for the families we work with is the opposite of “wide-angle”: we make portfolios built around one household’s circumstances, taxes, timelines, and appetite for exactly the kind of volatility described above. We keep that roster of clients deliberately small, because that sort of attention doesn’t scale. If you’d like to talk about what it would look like for you, Aubrey Ford will make the time.

Defense Reindustrialization Goes Global

Perhaps the least cyclical piece of that policy tailwind is defense, and its scale is easy to under-appreciate from a U.S.-centric vantage point. Morgan Stanley estimates Asian defense spending reached about $700 billion in 2026 — 1.8% of regional GDP, the highest share since at least the early 1990s — growing at a 6.6% annual clip since 2022, up from 4.5% in the prior decade. If the region’s stated commitments are met, that figure climbs toward $1–1.2 trillion, with Korea aiming for 3.5% of GDP, Taiwan 5%, and India 2.5% — and with the capital-expenditure slice, that is, the actual hardware orders that flow to industrial firms, growing from roughly $260 billion toward as much as $570 billion by 2030. Layer NATO on top, where members have signed up to a 5%-of-GDP framework (3.5% core defense plus 1.5% of broader security spending), with the U.S. administration openly pressing allies to carry more of the load. This is a genuine second leg — largely uncorrelated to the AI trade and underwritten by sovereign balance sheets rather than the credit cycle.

Of course, defense is, historically, a low-productivity use of capital, though it does come with an offset that is difficult to quantify: a good share of general-purpose technology, from GPS to the internet to drones, traces back to military spending, and AI looks likely to extend that pattern. Further, this is government-funded demand. U.S. net interest costs now run ahead of U.S. defense spending outright, and while much of Asia has the fiscal room to sustain higher budgets, the bill for a global rearmament eventually arrives in the bond market. Durable is not the same as free. There will be eventual consequences to a major bolus of military spending… though of course, the productivity its general-purpose technologies enable may make up for a great deal of it.

Here is something we would underscore for investors thinking about how to approach the trade of an industrial renaissance, who are tempted to buy “defense” as a single blanket idea. A great end-market does not a great company make. Nowhere is that clearer than in European defense, where the demand story is close to unimpeachable — order books at multi-decade highs, political will finally present — and yet the businesses filling those order books are, with a handful of exceptions, not being run as though they know it. The European primes remain fragmented national champions, slow thanks to politicized procurement, hemmed in by export rules, and content to let a large share of rising European budgets flow toward American hardware rather than aggressively build capacity and margin at home. The theme is one of the best of the decade. Many of the vehicles for it are, disappointingly, just indifferent compounders. A great end-market and a great company are not the same investment — and in European defense the two part ways.

So, What Might Belong on a Buy List?

To sum up: the picture is less a narrow technology rally than a broad industrial one, arriving through two doors at once: the physical requirements of the AI build-out through the first, and a policy-driven reindustrialization-and-rearmament wave through the second. The crowded, expensive, much-worried-about layer is the semiconductors, especially memory. The other layers of the economy being quietly pulled along behind them — power, components, materials, and the broad range of businesses that make up the industrial base — could be more attractive. In many cases, these companies’ stock prices have moved up, but we can expect pullbacks; we are researching many opportunities to add to our buy list.

Have Children or Grandchildren? Here Is Something You Can Do Today That Can Pay Off Big

A last aside for parents and grandparents: the “Trump accounts” are now live. For U.S.-citizen children born between January 1, 2025 and December 31, 2028, the government will seed $1,000 — invested in a broad U.S. equity index — once a parent or guardian opens the account and files the election. Families can then add up to $5,000 a year; any child under 18 is eligible to hold an account. The structure is a traditional IRA: contributions compound tax-deferred and the account converts to a standard traditional IRA at 18. The seed and all gains are taxed as ordinary income on withdrawal; the family’s own after-tax contributions come back untaxed. In our view, the program will quietly turn a generation into shareholders, and channel a modest, steady bid into domestic equities — and will double as a deliberately visible advertisement for the rewards of owning American capitalism at a moment when skepticism of markets runs high among some younger voters. We suggest all families with children take advantage of this program. Click here to learn how.

Thanks for listening; we welcome your calls and questions.

General Disclosures About This Newsletter

The publisher of this newsletter is Guild Investment Management, Inc. (GIM or Guild), an investment advisor registered with the Securities and Exchange Commission. GIM manages the accounts of high net worth individuals, trusts and estates, pension and profit sharing plans, and corporations, among other clients.

Your receipt of this newsletter does not create a personal investment advisory relationship with GIM although some recipients may also be advisory clients of GIM. GIM has written investment advisory agreements with all its personal advisory clients, which sets forth the nature of that relationship.

The newsletter makes general observations about markets and business and financial trends and may provide advice about specific companies and specific investments. It does not give personal investment advice tailored to the needs, objectives, and circumstances of individual readers. Whether investment ideas and recommendations are suitable for individual readers depends substantially on the personal and financial situation of that reader, which GIM, as the publisher of the newsletter, makes no effort to investigate.

GIM attempts to provide accurate content in its newsletters to the extent such content is factual rather than analysis and opinion, but GIM relies primarily on information compiled or reported by third parties and does not generally attempt to independently verify or investigate such information. Moreover, some content and some of the assumptions, formulas, algorithms and other data that affect the content may be inaccurate, outdated, or otherwise flawed. GIM does not guarantee or take responsibility for the accuracy of such information.

Please note that investing in stocks, other securities, and commodities is inherently risky, and you should rely on your personal financial advisors and conduct your own due diligence in connection with any investment decision.

A Special Comment for Guild’s Clients

If you are an investment advisory client of GIM who is receiving this newsletter, please note that the fact that a general recommendation is made of a particular security, commodity, or investment area to its newsletter subscribers does not mean that investment is suitable for you or should be purchased by you. For example, GIM may already have purchased such securities on your behalf or purchased securities in the same industry (and an increase in the position for you may represent too much concentration in one security or industry), or GIM may believe the investment is not suitable for you based on your risk tolerance or other factors. If you have questions about the recommendations in this newsletter in relation to your account at GIM, please contact Tony Danaher, Rudi von Abele, or Aubrey Ford.

Conflicts of Interest

As of the date of this newsletter, GIM’s investment advisory clients or GIM’s principals owned positions in areas that are the subject of current recommendations, commentary, analysis, opinions, or advice, contained in this newsletter.

GIM and its principals have certain conflicts of interest in its relations with its investment advisory clients and its newsletter subscribers resulting from GIM or its principals holding positions for its clients or themselves which are also recommended to its clients. GIM may change the positions of its clients or GIM’s principals may change their positions (increasing, decreasing, and eliminating them) based on GIM’s best judgment at any given time, including the time of publication of the newsletter. Factors that lead GIM to change or eliminate its positions may include general market developments, factors specific to the issuer, or the needs of GIM or its advisory clients. From time to time GIM’s investing goals on behalf of its investment advisory clients or the personal investing goals of GIM’s principals and their risk tolerance may be different from those discussed in the newsletter, and the investment decisions made by GIM for its advisory clients or the investment decisions of its principals may vary from (and may even be contrary to) the advice and recommendations in the newsletter.

In addition, GIM or its principals may reduce or eliminate their positions in an investment that is recommended in the newsletter prior to notifying the newsletter subscribers of such a reduction or elimination. The publication by GIM of a “target price” or “stop loss” for a particular security or other asset does not necessarily represent the price at which GIM intends to sell or will sell any such assets for its advisory clients or the price at which GIM’s principals intend to sell any such assets.

As a consequence of the conflict of interest, GIM’s clients or principals may benefit if newsletter subscribers purchase assets recommended by GIM since it could increase the value of the assets already held by GIM’s investment advisory clients or GIM’s principals. On the other hand, GIM’s principals and clients may suffer a detriment if they seek to acquire additional shares in securities that have been recommended and the price of the securities has increased as a result of purchases by newsletter subscribers.

To help mitigate these conflicts, GIM seeks to avoid recommending the securities of individual companies where GIM or its principals have an ownership position and where the issuer is small or its securities are thinly traded. That way sales by GIM in advance of possible sales by newsletter subscribers would not be likely to cause any significant decrease in the sale price to newsletter subscribers. GIM has a fiduciary relationship with its investment advisory clients and cannot agree on behalf of such clients to refrain from purchases or sales of a security mentioned in the newsletter for a period of time before or after recommendations for purchases or sales are made to its newsletter subscribers.

GIM encourages you to do independent research on the securities or other assets discussed or recommended in the newsletter prior to making any investment decisions and to be especially cautious of investments in small, thinly-traded companies, which are usually the most risky investments that you can make.

Disclaimer of Liability

GIM disclaims any liability for investment decisions based upon recommendations, information, or opinions in its newsletters. GIM is not soliciting you to execute any trade. Nothing contained in GIM’s newsletters is intended to be, nor shall it be construed as an offer to buy or sell securities or to give individual investment advice. The information in the newsletter is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation, or which would subject GIM to any registration requirement within such jurisdiction or country.

COPYRIGHT NOTICE

Guild’s current and past market commentaries are protected by U.S. and international copyright laws. All rights reserved. You must not copy, frame, modify, transmit, further distribute, or use the market commentaries, without the prior written consent of Guild. This email or any download from a secure website is meant for only the intended recipient of the transmission, and may be a communication privileged by law. If you received this email in error, any use, dissemination, distribution, or copying of this email is similarly prohibited. Please notify us immediately of the error by return email and please delete this message from your system. Although this email and any attachments are believed to be free of any virus or other defect that might affect any computer system into which it is received and opened it is the responsibility of the recipient to ensure that it is virus free and no responsibility is accepted by Guild Investment Management for any loss or damage arising in any way from its use.

0 Comments